Q2 in Bitcoin and Crypto: Key Trends, Patterns, and What to Watch in Q3

Hello!

Today is July 9, 2026, and it is the 4,868th day that Bitcoin has been operating 24/7 without any hiccups.

This is the Q2 2026 Quarterly Overview from Dessenter – the second one, built from months of weekly coverage in our Lithuanian newsletter, and distilled for a global audience. It's for investors, builders, and curious professionals who want to stay on top of Bitcoin and crypto without drowning in noise. If you don't have time to follow the market daily but don't want to miss what matters – this is your shortcut.

Each section opens with a quick summary, followed by key trends and patterns, and closes with what to watch in Q3. This overview covers 17 categories – from regulation and stablecoins to AI agents, mining, DeFi, tokenisation, and beyond.

Expect these quarterly. If you find them useful, subscribe below to be notified when a weekly English edition launches.

Thanks!

Note: You'll receive a confirmation email in Lithuanian — just click the button to confirm. Our English edition is coming soon.

Author's analysis, AI-assisted drafting.

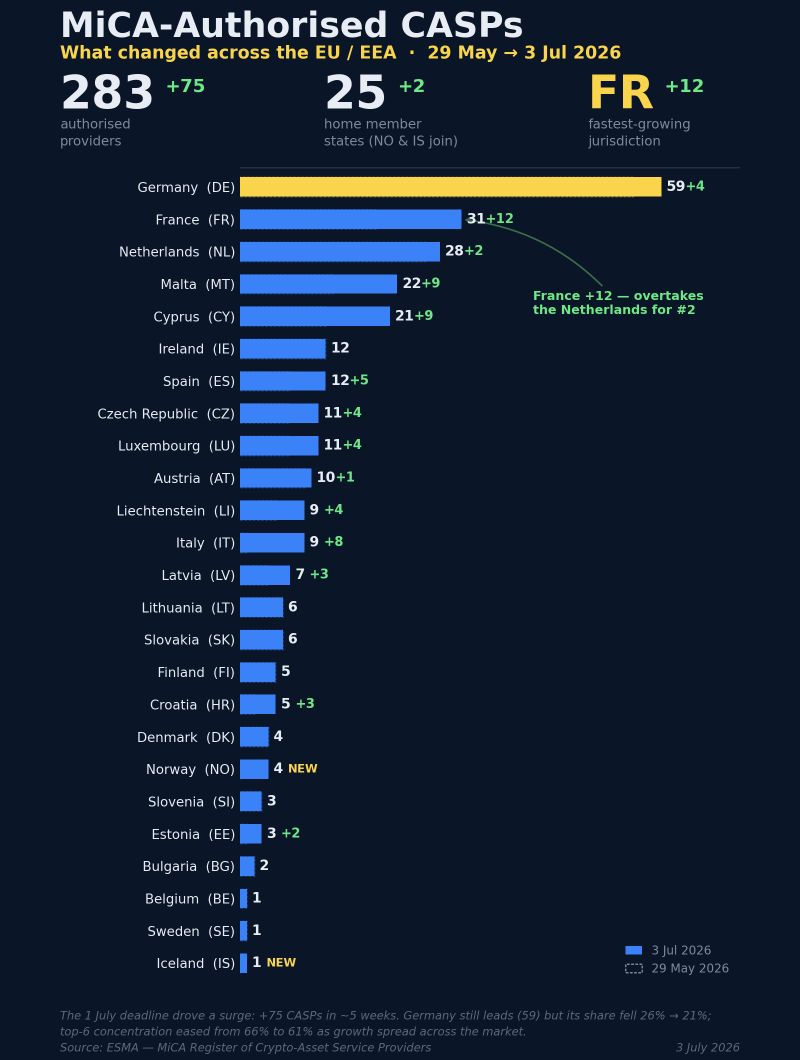

Regulation

Two deadlines defined the quarter: the July 1 cutoff under MiCA, the EU’s crypto-market rulebook, grew real teeth, while the US Clarity Act limped toward a July 4 target it was set to miss.

From Q1 to Q2

Q1 left the US bill stuck on the stablecoin-interest clause, with Coinbase blocking and Circle lobbying; Q2 added a hard July 4 target, and analysts’ ~30% passage odds were looking about right – at quarter-end, four political disputes were still unresolved, and the target was all but gone. On the EU side, Q1’s licensing ramp (170+ MiCA licenses) gave way in Q2 to enforcement as the July 1 transition deadline closed in.

Key trends & patterns

The quarter’s clearest split ran between enforcement power and enforcement outcome. MiCA’s July 1 cutoff gave regulators real teeth – the EU markets watchdog ESMA confirmed unlicensed firms cannot onboard new EU clients afterward – yet estimated roughly 60% of EU users were still on unlicensed platforms in late June. OKX Europe expects about 80% of exchanges not to survive, and Poland’s president vetoed MiCA transposition for a third time, leaving it the lone EU holdout. The US Clarity Act never got that far: four unresolved political disputes at quarter-end left its July 4 target effectively dead. Enforcement, meanwhile, hardened and turned on exchanges directly – the UK’s HTX sanction was the first time bank-style sanctions hit a crypto exchange, the EU’s 20th sanctions package banned dealings with Russian and Belarusian crypto providers and DeFi platforms (an 11-platform 21st package is in preparation), and US H1 2025 AML fines topped USD 1bn even as crypto-specific penalties collapsed 97%. Pulling the other way, a US Labor Department proposal would open 401(k) retirement plans to crypto – the largest single pipeline item of the quarter, still a proposal, that faces intense bipartisan and political pushback. A tax-tightening wave swept jurisdictions at the same time: Germany, South Korea, Japan, Illinois, plus EU exploration of harmonized capital-gains rules and a transaction levy. And stablecoins and central bank digital currencies (CBDCs) moved to the center – the Bank of England replaced account caps with an issuance-cap regime, the European Parliament advanced the digital euro, and the US moved to ban a CBDC by 2030.

What to watch in Q3

- Does the Clarity Act clear its four open disputes and reach a Senate floor vote before the autumn recess, or slip into 2027?

- Post–July 1, does ESMA enforcement actually move the ~60% of EU users from unlicensed platforms, and does Binance secure a license?

- Does Poland finally transpose MiCA, or does the EU open infringement proceedings against its last holdout – and does the MiCA-2 consultation (closes August 31) produce concrete stablecoin reserve-rule relief?

- Do the Bank of England’s stablecoin issuance cap and the US CBDC ban move from proposal to signed rule?

Adoption

Usage kept climbing while price fell – adoption decoupled from the bitcoin chart, carried by stablecoins, cards and bank rails – even as a new generation of BTC payment infrastructure shipped.

From Q1 to Q2

Q1's headline was Square rolling automatic BTC payments toward a 4m-merchant base; Q2 delivered the activation – over 1m US businesses live – and added a card signal: monthly cryptoasset card-payment volume tripled year-on-year to ~USD 600m by March, while a widely circulated May figure of USD 7.8bn measures cumulative volume, 230% more than a year ago.

Key trends & patterns

The adoption vector is moving from bitcoin itself to stablecoins and tokenization – Bitwise reports advisors now prefer both over bitcoin – and the pattern shows up across every rail: merchant enablement, card volume (roughly 90% of it over Visa rails) and ownership all climbed as bitcoin fell toward USD 60K, meaning blockchain-powered tech growth is routing through non-Bitcoin infrastructure rather than the asset itself. Banks and brokerages kept opening the front door: Charles Schwab launched retail BTC/ETH trading, Banca Sella became the first Italian bank licensed under MiCA to offer cryptoasset services (rollout due later this year), and JPMorgan's Kinexys blockchain platform breached USD 3tn cumulative volume at ~USD 5bn/day – and even a central bank joined the chorus, the Czech governor telling the Bitcoin2026 stage that a small BTC allocation improved his bank's portfolio math (BTC has fallen more than 20% since the speech). The commercial payments market widened in parallel: Tether and Fasset launched a Visa card that spends tokenized gold (XAUT converted to USDT at checkout, up to 6% cashback), Blockchain.com opened a stablecoin payments platform for Brazilian businesses, KuCoin plugged its network into Mexico, Bangladesh and Zambia, Ripple bought into African payments through Flutterwave, and Mizuho warned that a successfully launched X Money – especially with cryptocurrency payments integrated – could seriously accelerate competition. Emerging-market momentum continued too (Bahrain's settlements, a Vietnamese proposal to accept cryptoassets as SME loan collateral, Korean and Japanese public-sector initiatives), while GameFi's collapse stood as the counter-signal – the speculative on-chain consumer use case largely evaporated.

The quarter's most underreported story, though, was BTC payment tooling shipping in bulk. The Ark protocol – which both complements and competes with Lightning – reached the Bitcoin mainnet through the Second team's Bark tools, aimed squarely at payments (with Ark Labs covering financial products), at the cost of more third-party trust and weaker privacy than Lightning; wallets are already integrating it. Spiral opened testing of LDK Server, letting developers run their own Lightning nodes and become service providers; Cashu's new design further cut the trust users must place in its mints; Wasabi turned its Coinjoin history-cleaning into a way to actually pay; and miner GoMining launched an onchain-only payments SDK that routes confirmation straight into its mining pool – instant and fee-free for the payer, 0.2% for the business. The catch is demand: a Swiss central bank survey found only 0.4% of cryptoasset-holding residents used it for payments last year. The rails are being built faster than they're used – which is why the tax fight matters, with the Cato Institute joining bitcoiners in calling capital-gains tax on small BTC payments nonsense while the US Congress fights over an exemption.

What to watch in Q3

- Does Square enablement climb from >1m toward 4m, and does any actual usage figure (not just activation) surface?

- Do the new BTC rails find users – Bark in major wallets, LDK Server past testing, GoMining beyond its ten pilot businesses – or does the Swiss pattern (infrastructure without payments) hold, and does the US small-BTC-payments tax exemption advance?

- How will the bear market affect banks' plans to roll out cryptoasset services or seek licenses, such as under MiCA – and cryptoasset ownership among retail investors?

- Will X Money integrate BTC, stablecoin, and or/crypto payments?

AI agents

Agentic payments crossed from demo to measurable scale – almost entirely on stablecoins and cards for now, while bitcoiners made the case for BTC as the neutral, decentralized, global rail the agent economy will eventually need, something no stablecoin can offer.

From Q1 to Q2

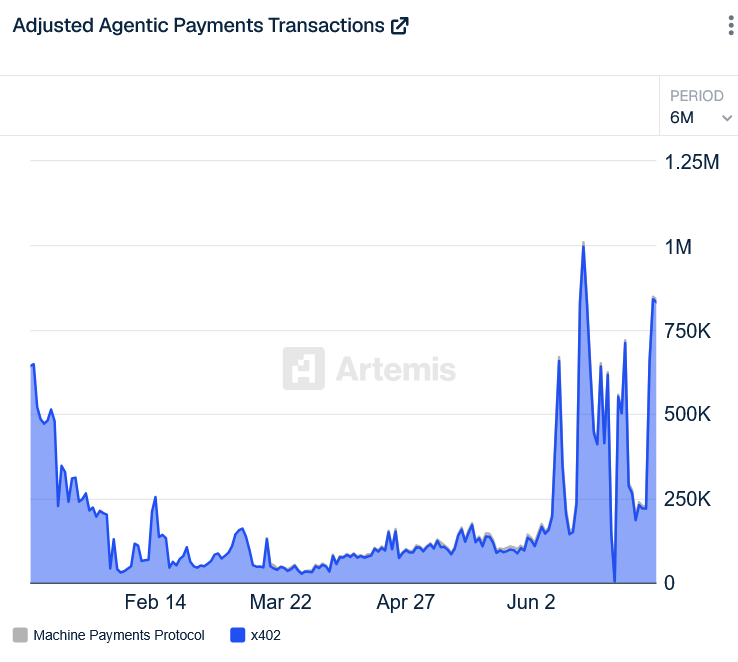

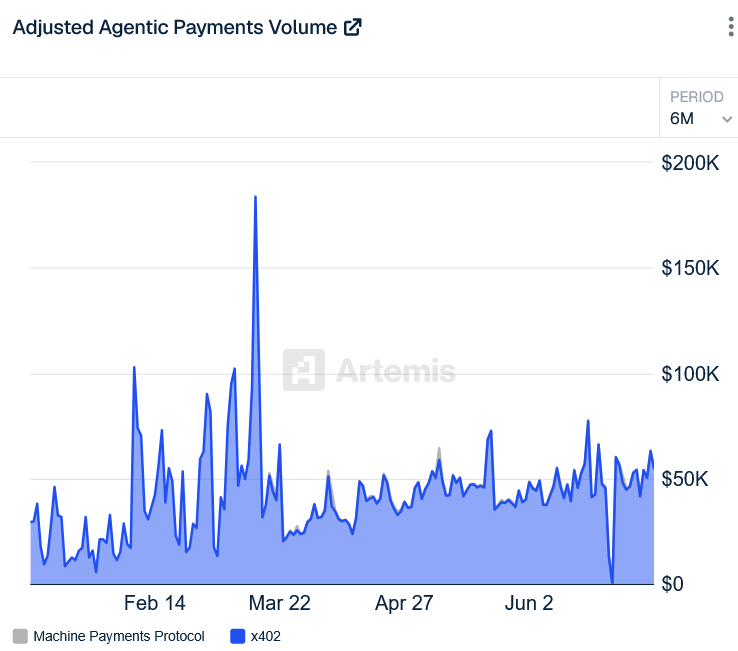

Q1’s open question was whether Coinbase’s x402 stablecoin protocol could gain enough adoption to matter; Q2 answered it – x402 logged 100m agent operations on Base over nine months, with transactions above USD 1 jumping from 49% to 95% of the total.

Key trends & patterns

The most telling pattern is what’s missing: every major agentic-payment rail this quarter – x402, Visa Intelligent Commerce, Mastercard Agent Pay, AWS x402, plus MoonPay, OKX and TON protocols – runs on stablecoins or cards, not bitcoin; understandably, the Coinbase/Tempo agentic-payments report didn’t mention bitcoin at all. The scale is real: x402’s 100m operations and a 49%→95% value share sit alongside a 400% Q1 jump in AI-platform traffic to US merchant sites – measurable volume, not test traffic. Exchanges moved to meet the trend, opening customer accounts to agents – Coinbase for Agents (connecting ChatGPT/Claude), MetaMask, Robinhood third-party agents, Gemini agentic trading – alongside heavy capital and infrastructure inflow. One counter-thesis is worth stating plainly – as Spiral argued in May, bitcoin remains the only neutral, maximally decentralized settlement layer an agent economy could standardize on – the niches centralized rails can’t take are exactly where BTC still has a claim. The counterweight is security: an agent wiped a startup’s database, malicious instructions surfaced during agent browsing, and payment routers were flagged as a new attack surface. The risk is structural, and the safeguards are not keeping pace.

What to watch in Q3

- How will the competitive dynamics among fiat, stablecoins, crypto, and Bitcoin change, and which use cases will each of these rails dominate?

- Do exchange agent-access products (Coinbase for Agents, Gemini) report real user volume, or stay in limited preview?

- Does any regulator move on AI-agent financial liability after Q2’s failure cases?

Blockchains

A governance-and-audit reckoning: Ethereum shrank its own Foundation, Bitcoin fought over non-financial data and quantum defense, and multiple chains discovered they’d been quietly mintable “from air.”

From Q1 to Q2

Q1 pointed at Ethereum’s roadmap milestones and a Bitcoin hashrate question; Q2 reframed both. The Ethereum conversation moved from shipping features to restructuring the institution behind them – Vitalik Buterin refocusing the Foundation on censorship-resistance, openness, privacy and security and cutting its size – while Bitcoin’s energy went into governance fights and preparing for the post-quantum era.

Key trends & patterns

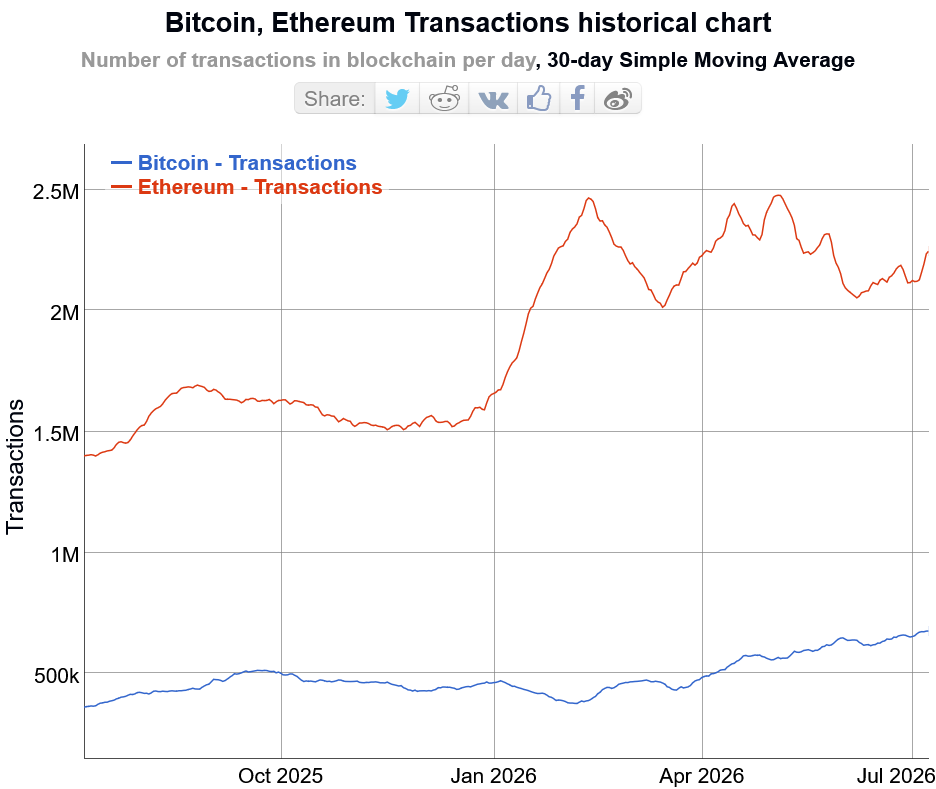

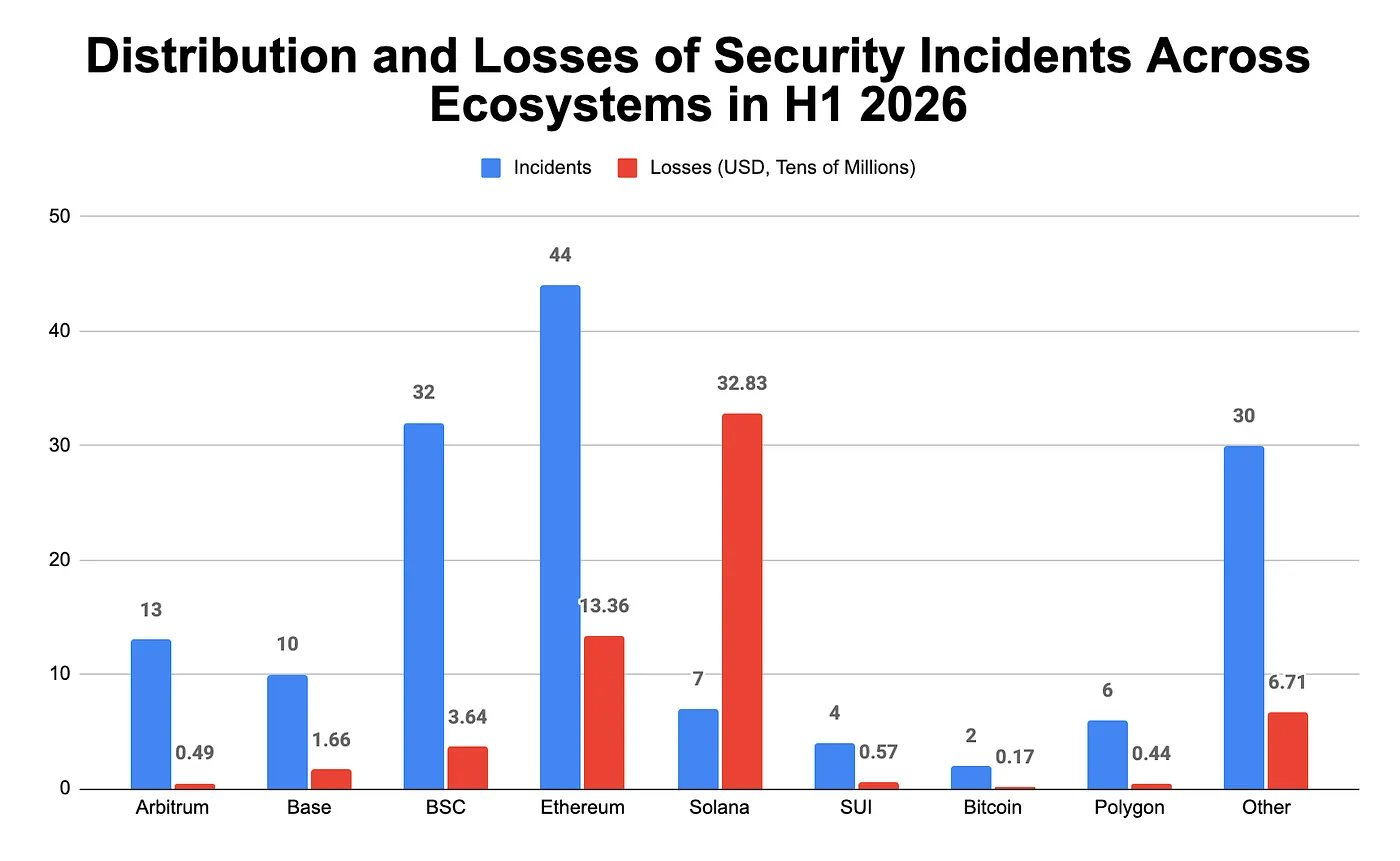

The throughline was maturation pain, not expansion. Ethereum’s Foundation entered open contraction – Buterin reducing his own influence, a 20% staff cut, a sharply reduced budget, visible departures, and David Hoffman, a prominent Ethereum advocate, selling his ETH as the “ETH is money” thesis ran out of air – a microcosm of the broader decline in crypto developer activity. Bitcoin turned inward into two governance battles: the Bitcoin Knots push behind BIP-110 (a Bitcoin Improvement Proposal) to limit non-financial data – images and other non-payment content stored on the chain – with a long-warned (and widely doubted) August Bitcoin blockchain-split risk; and the BIP-361 proposal to freeze ~5.6m quantum-vulnerable BTC, opposed by Blockstream’s Adam Back and much of the base. A run of security disclosures – a proven denial-of-service path on testnet, an 8-year-old Bitcoin Core bug, a v31.0 privacy gap – reinforced the audit theme, sharpened by “from-air” minting bugs: the Litecoin flaw exploited in March and probed again in April, and a Zcash bug surfaced with AI assistance (Monero’s audit still pending). Beneath the headlines, reliability cracked: Sui stalled three times in two days and Base twice, with centralization blamed among other things. Solana was trying to mature past its memecoin image with the Alpenglow upgrade planned for Q3.

What to watch in Q3

- Does BIP-110 hit its August support threshold or trigger the long-warned Bitcoin blockchain split – and does the contested eCash hard fork (estimated around August 21) land as an event or a footnote?

- Does Ethereum’s next upgrade, Glamsterdam, hold its H2 2026 target after the EF budget and headcount cuts, and does the ecosystem close the developer-funding gap the Foundation’s retreat opens?

- Does Solana ship Alpenglow on schedule, and does its tokenized-asset base keep climbing?

- Do more “from-air” audit findings surface – specifically, does the pending Monero audit return anything?

Stablecoins

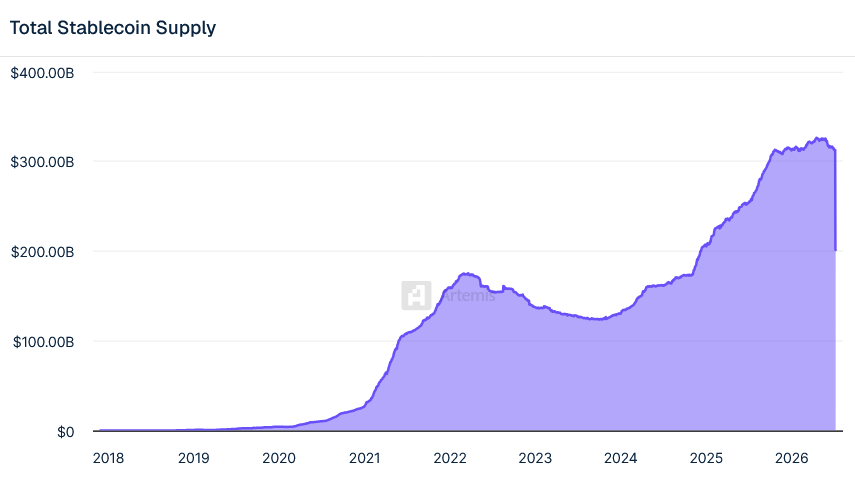

Stablecoins were the quarter’s consensus winner – over USD 322bn in cap, pulling banks, fintechs and AI agents onto tokenized fiat rails – yet still 99% dollar and overwhelmingly B2B.

From Q1 to Q2

Q1 flagged the SEB/Qivalis euro stablecoin, US stablecoin legislation, and a possible USDT-on-Bitcoin move. Q2’s answer was lopsided: the euro consortium grew ahead of the launch, US law stayed stuck, and the dollar’s grip tightened rather than loosened – non-dollar stablecoins were still just USD 771m, 0.24% of the market.

Key trends & patterns

The B2B tilt intensified: Paybis reported 98% of its Q1 stablecoin payments came from business clients, up from 36% in 2023 – a sharp jump from Q1’s own finding that only 7% of total stablecoin volume reached real commerce. That skew persists even as the rails scaled to mainstream size: stablecoins surpassed the US Automated Clearing House in February (USD 7.2tn vs USD 6.8tn; compared with Visa’s USD 1.2tn). Market cap surpassed USD 322bn – more than the foreign reserves of 95 countries, 99% dollar-denominated – with Chainalysis projecting USD 1,500 trillion in annual volume by 2035. Distribution built genuine retail rails even if usage hasn’t followed: Cash App, SoFi’s national-bank SoFiUSD, Western Union USDPT on Solana, MoneyGram MGUSD on Stellar, Mastercard USDC/PYUSD settlement, Meta paying creators in USDC, and a Stripe/Visa/Mastercard joint platform. Europe kept trying: the Qivalis consortium expanded toward an H2 2026 euro stablecoin launch, Société Générale and Japan’s three megabanks moved, yet non-dollar stablecoin share barely registered. The quarter also kept demonstrating what these overhyped rails cost: Circle failed to freeze the Drift thieves’ USDC and was sued in a class action for it, yet both Circle and Tether froze millions at state request – at times hurting innocent companies – a running reminder that stablecoins are not your money. Regulators, meanwhile, kept reaching for fund analogies rather than money – the BIS – the central banks’ bank – compared stablecoins to ETFs, the Atlanta Fed to narrow banks, the ECB’s Isabel Schnabel to money-market funds – even as the Bank of England went the other way and treated them as a new form of money, and MiCA’s stablecoin reserve friction persisted.

What to watch in Q3

- Does Qivalis actually ship a euro stablecoin in H2, or slip into 2027?

- Does the non-dollar stablecoin share move off 0.24%, or does the dollar’s 99% simply harden?

- How will increasing stablecoin market fragmentation and frozen funds affect the use of stablecoins for payments?

- Does any US stablecoin framework pass after the summer miss?

Like what you're reading? A weekly English edition is launching soon — free for the first 21 days. Get notified:

Note: You'll receive a confirmation email in Lithuanian — just click the button to confirm. Our English edition is coming soon.

Companies

The treasury-company model met its first real drawdown – Strategy briefly held more bitcoin than the largest ETF, then disclosed another multibillion-dollar paper loss and started selling BTC, while ETH treasuries sank deeper into red as well, and layoffs, delayed IPOs, and M&A reshaped the field.

From Q1 to Q2

Q1 had us watching Kraken’s IPO, Strategy’s buying pace and its STRC financing. Q2 delivered the stress test: Strategy kept buying – USD 2.54bn in a single week, before testing the market with a BTC sale, as the price fell below USD 60K, putting visible strain on its preferred stock, STRC, and the broader IPO pipeline split between movers (Securitize) and delayers (Kraken, Consensys, and – per unconfirmed reports – Grayscale).

Key trends & patterns

The Q2 stress didn’t land evenly across the field: businesses that move money stayed profitable, while businesses exposed to bitcoin’s and ethereum’s balance sheets took the damage. As revealed in Q2, Tether posted USD 1.04bn in Q1 net profit, and Circle grew revenue to USD 694m (+20%) on USD 21.5tn of operational volume (+263%), while Kraken booked USD 507m revenue but watched EBITDA collapse from USD 168m to USD 18m, and BitGo took a ~USD 61m loss, despite revenues more than doubling. Strategy sat at the sharp end of that same split: for the first time since Q2 2024, it briefly held more bitcoin than the largest ETF after a USD 2.54bn week – then disclosed a USD 12.54bn Q1 paper loss, made its first BTC sale since 2022, and saw its cash reserves shrink and STRC preferred shares slide under forced selling. By late June, the market was openly debating whether the strategy could become this cycle’s Terra/Luna (the 2022 collapse that erased tens of billions), but the consensus is that it is not. Either way, STRC – which funded the majority of this year’s bitcoin purchases – broke from its price target, and analysts split between a self-stabilizing dividend fix and forced BTC sales. By the start of Q3, though, the company seemed to have stabilized the situation. Equities punished the model broadly (Metaplanet and MSTR down sharply year-on-year), and European replication looked doubtful; the one clean positive was SpaceX confirming a BTC 18,712 portfolio – larger than earlier estimates. ETH treasuries fared badly as well – 15 listed names sat on combined losses exceeding USD 1.4bn even as BitMine kept accumulating. Underneath, consolidation accelerated: an M&A and mega-raise wave (building on Q1’s Mastercard/BVNK at USD 1.8bn alongside layoffs and outright failures – Bitcoin Depot bankruptcy and Binance’s Lithuanian entity closing.

What to watch in Q3

- Will Strategy manage to bring STRC back to USD 100, and will it keep its promise to buy 20 BTC for every bitcoin it sells?

- If the bear market persists and/or deepens, how will it affect product shipments?

- Will layoffs and M&A consolidation accelerate as weaker players run out of runway?

Exchanges

MiCA’s July 1 cutoff turned into a survival filter in the EU, and the exchanges that expect to clear it spent the quarter racing to become full-stack financial firms.

From Q1 to Q2

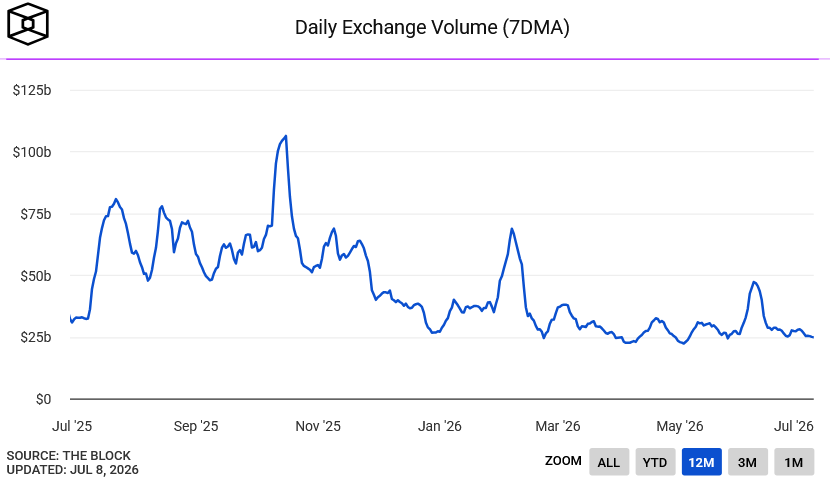

Q1 had compliance churn and a licensing ramp; Q2 made it existential. MiCA’s July 1 deadline closed in with an estimated 60% of EU users still on unlicensed platforms, and OKX Europe projecting that ~80% of exchanges won’t survive MiCA, Binance ended the quarter without a MiCA license, and spot volume kept falling by 19%, to around USD 3tn.

Key trends & patterns

The diversification pivot is still more strategy than proof: exchanges raced into derivatives, tokenized assets and payments, but the one clear test of real-world traction – the SpaceX tokenized-stock campaigns – got pulled, not scaled. MiCA worked as a filter, already producing real casualties: survivors relicensed through accommodating jurisdictions (Poland’s Kanga via Latvia), while Binance missed the cutoff due to a seemingly politicized licensing process – and its rivals immediately courted its EU clients. Diversification away from spot fees ran in parallel. Coinbase expanded into derivatives, payments, and an AI advisor (despite a Q1 loss, an AWS outage, and a French data breach); OKX and ICE formed the OKXICE joint venture for futures and tokenized stocks; Bybit and Blockchain.com pushed tokenized-asset products. The full-stack thesis has evidence beyond product launches: the BIS warned that big exchanges now operate as shadow banks – lending and yield without deposit insurance – and Binance’s own research shows a meaningful share of its clients using the platform for savings and payments, not just trading, mostly in emerging markets. Consolidation and strategic stakes deepened – Deutsche Börse into Kraken, plus a wave of Korean deals (Hana/Dunamu, Samsung, OKX). Trust friction ran underneath it all: the RAVE manipulation episode, the Coinbase breach, and a >40-exchange Transparency Alliance forming in response. Binance set a 3-billion-user 2030 goal against >320m users today and added a 7-day withdrawal delay for physical-attack protection.

What to watch in Q3

- How will the EU crypto exchange market actually change, and will multiple exchanges still serve EU clients even without licenses?

- Which jurisdiction will be brave enough to grant Binance a license despite the rumored pressure from the ECB?

- How successful will the tokenized-stock and derivatives push be, and will TradFi giants increasingly join this bandwagon?

- Does the OKXICE joint venture clear regulators and launch?

Wallets

Wallets hardened along two axes – self-custody and privacy – under regulatory pressure, while AI moved inside them.

From Q1 to Q2

Q1 had us watching for a Morgan Stanley wallet and more IBAN+BTC services. We’ll need to wait longer for Morgan Stanley, but bitcoiners were offered more opportunities to manage their bank accounts and BTC services in a single wallet. Also, the quarter’s movement came from incumbents tightening privacy (silent payments, Payjoin, Coinjoin) and pushing users toward self-custody as regulatory pressure mounted.

Key trends & patterns

Self-custody and privacy are converging into one regulatory response, with AI layering in as a separate, faster-moving vector. First, a self-custody migration driven by regulation: Wallet of Satoshi moved business payments to self-custody, and Club Orange handed key control to users. Second, privacy as the active development frontier – Sparrow added silent payments, Bull Bitcoin strengthened Payjoin, and Wasabi began experimenting with Coinjoin payments. Third, AI entered the wallet: a user recovered five BTC after eleven years with AI assistance, and Alby Hub added agent capabilities. Hardware refreshed (a new Bitkey model with a screen, the Coldcard M5), but the notable security note was a medium-severity flaw disclosed in the Trezor Safe 7 – bypassing one protection layer without enabling actual theft, to be patched by year-end. One current runs the other way: Exodus repackaged its wallet as a mainstream payments app. Regional builders stayed active, including Lithuania’s Wave.space raising its first round.

What to watch in Q3

- Does privacy tooling (silent payments, Coinjoin, Payjoin) move from niche to default in mainstream wallets?

- Does AI-in-wallet expand past recovery and agent demos into new shipped consumer features?

- Does Morgan Stanley or any other traditional finance giant actually launch a wallet, or stay with trading-only access?

DeFi & CeFi

DeFi and CeFi absorbed the year’s two biggest thefts and proved structurally resilient, even as BTC-native DeFi retreated and AI-enabled attacks became the sector’s defining new fear.

From Q1 to Q2

Q1 pointed at Aave v4 shipping and BTC-native DeFi gaining traction; Q2 delivered the launch but inverted the BTC thesis. Aave v4 went live on Ethereum, while the quarter was defined by two record thefts in quick succession – Drift losing over USD 280m in early April, the year’s record at the time, North Korea suspected, then the Kelp DAO exploit days later topping it – and by BTC-native DeFi retreating rather than advancing.

Key trends & patterns

Bitcoin’s role split in two this quarter, and the split is the story: BTC-collateral lending broadened – Strike, Aven, Coinbase UK loans, Roxom, with Zest announcing a non-custodial variant – even as BTC-native DeFi retreated, with Botanix shutting down and deployed BTCfi value sliding back; bitcoin is still being more held rather than worked, even as it was borrowed against elsewhere. The security stress test came in two blows. Drift’s >USD 280m loss drew a Tether-led rescue that pushed the platform from USDC to USDT; the Kelp DAO theft (USD 292m) sent value fleeing protocols across the sector and triggered coordinated stabilization, a legal fight over the frozen funds, and a verdict from Standard Chartered that the incident did not break DeFi. The system held. However, due to an overall slowdown in the cryptoasset industry, DeFi yields fell below TradFi yields, pushing capital toward traditional rates. AI-enabled attacks moved from concept to named threat: OpenZeppelin’s Aráoz warned no platform is safe, and researchers cautioned that next-generation AI models could be turned on DeFi protocols at scale. The convergence trend kept running (Stripe Tempo + Morpho, RedStone Settle), but the security narrative dominated – reinforced when Radiant Capital closed after a USD 50m theft.

What to watch in Q3

- Is Aave’s real BTC-backed lending proposal via Babylon advancing, and will Kraken keep pursuing its rumored plans to buy a stake in Aave?

- Does the deployed BTCfi value recover or keep sliding after Botanix?

- Are the warned AI-enabled exploits actually increasing, and does the industry manage to strengthen its protections?

Tokenization

Tokenization won the institutional argument – banks, asset managers and even longtime skeptics piled into tokenized funds, deposits and equities – though most of it is still traditional finance in a digital wrapper.

From Q1 to Q2

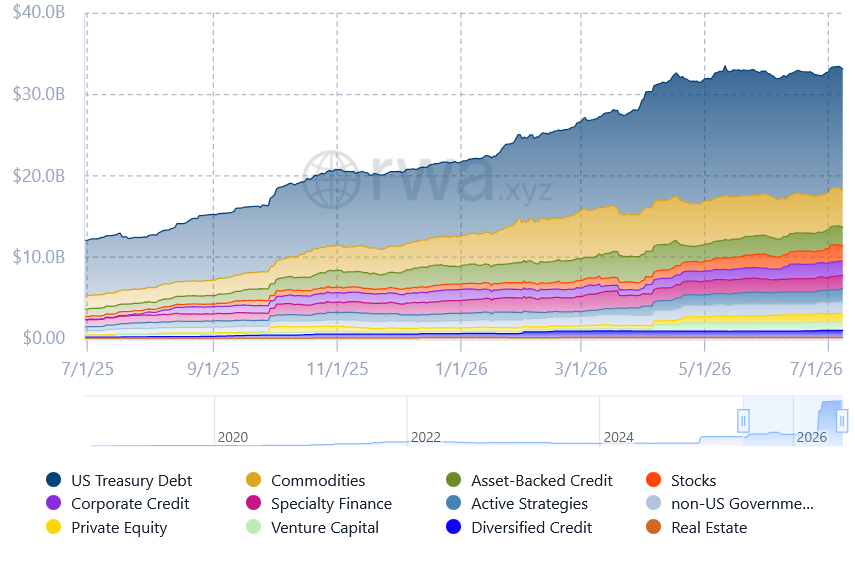

Q1 was pilots; Q2 moved from acknowledgment to scale within a single quarter – the IMF conceded tokenization’s benefits and risks, US settlement giant DTCC prepared platform trials, and by June the tokenized real world asset (RWA) market had grown to USD 65bn (+44% YTD), tokenized equities had jumped to USD 5.5bn (+147% YTD), and the biggest US banks had begun building a joint tokenized-deposit network.

Key trends & patterns

The institutional rush was wide but shallow, and the shallowness is the tell: Pantera estimated ~80% of tokenized projects are still just “newspaper online” – digital copies of existing products – even as Nouriel Roubini, a longtime crypto critic, joined a tokenized product anyway. The quarter offered both poles of that critique in miniature: Securitize’s deal with Computershare creates issuer-sponsored tokens that legally are the shares, while Bitget’s pre-IPO “stocks” are tokens with no claim on the company at all. That shallowness didn’t stop the numbers from climbing: RWA market sizing hit USD 65bn (+44%), with Ethereum securing about a third of it; tokenized equity was the fastest-growing class at +147%; and forecasts turned aggressive – Citi projects USD 5.5tn by 2030 (range USD 2.7–8tn), Standard Chartered USD 4tn by 2028, half of it stablecoins. The participant list reads like a TradFi roll call: State Street+ Galaxy, Fidelity, JPMorgan, Invesco and Franklin Templeton on funds; major US banks on a shared tokenized-deposit network (targeted H1 2027); Visa and Anchorage on deposits; BIS moving its wholesale-settlement project into live trials and a Chainlink-anchored bank coalition building real-time FX settlement. The one consumer-facing edge was tokenized collectibles (Pokémon cards posting sharp revenue growth), but the center of gravity is firmly institutional.

What to watch in Q3

- Does tokenized-equity’s +147% sustain, or was it a low-base spike?

- Do the major-bank tokenized-deposit network and the Chainlink-anchored FX-settlement coalition move from announcement to live rails?

- Will the industry offer more truly innovative tokenized products rather than digital copies of existing products?

Quantum

The quantum threat got somewhat more concrete enough to fight about – a real freeze proposal and a hard exposure number – but a botched “demonstration” showed the community’s messaging is as much a risk as the computers.

From Q1 to Q2

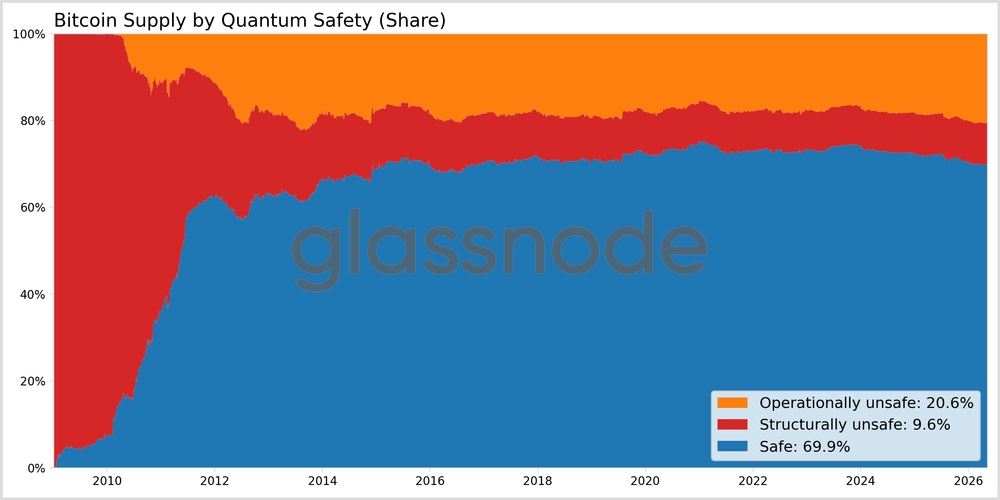

Q1 asked whether post-quantum proposals would advance toward actual adoption by the network and whether Google’s 2029 timeline would force a formal Bitcoin response. Q2 delivered proposals that hardened into a concrete and divisive plan – BIP-361, to phase-freeze vulnerable BTC including ~1m coins attributed to Bitcoin’s creator Satoshi Nakamoto – while Glassnode quantified the exposure at ~30% of supply (~USD 468bn) in addresses with revealed public keys, that, in theory, for now, would allow a quantum computer to derive private keys and steal BTC.

Key trends & patterns

The freeze proposal’s real fight isn’t about cryptography – it’s about the governance of Bitcoin. BIP-361 emerged as a concrete and divisive plan, with Jameson Lopp and five researchers on one side and Adam Back and much of the base opposing. Glassnode’s exposure estimate – ~30% of supply, ~USD 468bn, in addresses with revealed public keys – gave the debate its stakes. Defenses proliferated in parallel: a Lightning Labs recovery prototype, quantum-safe transaction schemes, and a quantum-resistant wallet from Postquant Labs. Hardware pressure rose – Microsoft’s Majorana 2 chip marked another reliability gain, AI-accelerated – and the advisory layer pushed harder, with Brink funding its first post-quantum grant and a Coinbase advisory group urging preparation now and clearer communication. That last point was the quarter’s bruise: post-quantum security solutions provider Project Eleven’s overstated “demonstration” became a communication crisis, criticized by a Google researcher, undercutting the credibility the field needs.

What to watch in Q3

- Does BIP-361 gain or lose support – does the freeze debate coalesce or fracture?

- How will BIP-360, which should prevent quantum computers from deriving private keys from exposed public keys, progress, and do any quantum-safe transaction standards move toward real adoption by the network?

- Does the next hardware milestone after Majorana 2 shorten the perceived timeline below 2029?

Mining

Major miners continued their AI pivot as it became the whole identity, funded by record bitcoin selling into a falling market.

From Q1 to Q2

Q1 raised the question of whether AI infrastructure spend would pay off and whether hashrate would recover; Q2 answered the first with “not yet, but all-in” and the second with “no.” Listed miners sold a record >BTC 32,000 in Q1 to fund AI capex, hashrate had already fallen for the first time in six years, and Bernstein tallied >27 GW of planned capacity behind >USD 90bn in AI contracts. Meanwhile, hashrate, or the computational power of the Bitcoin network, dropped by another 6%, after decreasing 7% in Q1.

Key trends & patterns

While the top of the industry rebrands, the base is quietly decentralizing – the quarter’s more revealing story. Even as listed miners fund a full-scale pivot into AI infrastructure, a parallel push emerged to decentralize the mining that remains. Major pools agreed to roll out Stratum V2 across roughly three-quarters of hashrate, solo miners kept winning blocks, and Tether released an open-source mining toolkit – real decentralization progress running directly counter to the consolidation at the top. State-level programs multiplied with opposite philosophies: Uzbekistan’s tax-free Karakalpakstan zone through 2035 courting miners, Oman mandating that licensed miners join its national Omanhash pool. Meanwhile, Canaan won a Nordic district-heating supply deal but posted a widening quarterly loss.

What to watch in Q3

- Does any listed miner report AI revenue that meaningfully offsets mining income, validating the pivot?

- Does hashrate resume climbing, stabilize, or keep sliding?

- Does Oman’s mandatory-national-pool model spread to other states, and does Stratum V2 deployment actually decentralize block construction more?

CBDC

The transatlantic split hardened: Europe advanced a digital euro toward law while the US moved to ban a CBDC outright.

From Q1 to Q2

The controversial digital euro moved from standards-setting – ECB signing payment-standard agreements – to political approval, with the European Parliament's Committee on Economic and Monetary Affairs blessing it ahead of July negotiations, alongside a pilot drawing strong applicant interest (final participant list due July). The US, meanwhile, set a CBDC ban by 2030 in motion (Donald Trump delaying the signing).

Key trends & patterns

What neither side has resolved matters more than the divergence itself: fresh research argues a CBDC must protect user privacy yet still requires trusting central banks – a tension sitting underneath both approaches. And they diverge sharply: Europe is building public digital money through its institutions in an attempt to protect itself from USD-backed stablecoins, while the US is legislating against the concept entirely.

What to watch in Q3

- Does the digital euro’s July negotiation between the European Parliament, the Council, and the Commission yield a concrete legislative timeline, or stall?

- Is the US CBDC ban actually signed, or does the delay persist?

- Does the digital euro pilot’s final participant list (July) signal real scope and ambition?

Privacy

Privacy became an open front – Europe moving against VPNs and private wallets, builders answering with trust-minimizing tools and censorship-resistant marketplaces.

From Q1 to Q2

Q1’s watch item was whether AMLA, the EU’s new anti-money-laundering authority, would publish private-wallet identification rules (scheduled July 2027, early signals expected in Q2). The Q2 signal arrived not as AMLA rules but as a broader clampdown – an EU VPN-restriction plan and a French proposal to require declaration of larger private-wallet holdings.

Key trends & patterns

The builder response wasn’t reactive tinkering – the tooling emerging this quarter is increasingly censorship-resistant by design, built to sit on ground regulators can’t easily reach. On the regulatory side, the EU floated VPN restrictions, France proposed a declaration requirement for larger private wallets, and age-verification debates fed the same VPN-limiting direction. On the builder side, Cashu’s Calle launched Europa, a VPN marketplace on Nostr, a decentralized communication protocol, while Martti Malmi shipped a registration-free Nostr VPN. Privacy building blocks advanced too: Starknet’s strkBTC, the proposed pERC-20 standard, and a StarkWare zero-knowledge KYC demo that proves compliance without full disclosure. Wallet-level privacy moved in step (Sparrow silent payments, Bull Bitcoin Payjoin, Wasabi Coinjoin – see Wallets).

What to watch in Q3

- Does France’s private-wallet declaration proposal advance, and do AMLA’s rules show concrete drafting ahead of the 2027 date?

- Is the EU VPN-restriction plan moving forward—and will Nostr-based solutions become a real countermeasure to worrying EU anti-privacy policies?

- Does zero-knowledge KYC move from StarkWare demo to a shipped product?

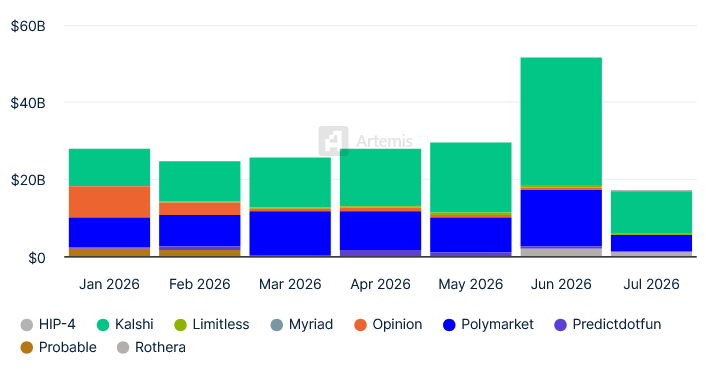

Prediction markets

Prediction markets kept scaling toward mainstream legitimacy while manipulation, insider trading, and gambling-economics critiques trailed close behind.

From Q1 to Q2

Q1 had a monthly volume past USD 20bn (~20x YoY), and Polymarket planning a major overhaul. In Q2, Polymarket launched IPO-prediction markets with Nasdaq Private Market, and Meta was reported to be building its own platform – even as Polymarket faced manipulation accusations and a regulator probe. Meanwhile, jurisdictions across the globe continue to block prediction markets.

Key trends & patterns

One number undercuts the institutional rush: research found only ~3% of trades reflect genuine probability estimates – the rest effectively fund the winners’ gambling – while a separate study put the format’s profitability threshold near USD 500k in turnover. Mostly gambling dressed as forecasting, even as the legitimacy push accelerated on every other front. On legitimacy: Polymarket’s planned exchange-style overhaul and its launched Nasdaq-linked IPO markets, JPMorgan hinting at bank entry, Meta’s reported Arena, and a 21Shares forecast naming prediction markets among crypto’s fastest-growing sectors. On the integrity side, the cracks showed in the same quarter – Polymarket hit with manipulation claims and a scam, a soldier charged with insider trading on Maduro-related contracts, and the Coinbase/Gemini New York lawsuit alleging illegal gambling.

What to watch in Q3

- Does monthly volume build on the USD 20bn+ base toward the 21Shares >USD 100bn/yr forecast?

- Does Meta’s reported platform launch, bringing a Big Tech distribution channel into the space?

- How will regulatory challenges affect the expansion of this sector?

Law & crime

The threat kept moving off-screen and onto the body: physical attacks on holders kept climbing, and AI began reshaping the fight – with the defenses, for now, the side posting real numbers.

From Q1 to Q2

Q1 logged 72 confirmed physical attacks in 2025 (+75% YoY), with Q1 2026 alone already at 23 or more; Q2 confirmed the trend wasn’t slowing – France alone reached at least 41 kidnappings year-to-date by late April, with 88 suspects charged. The “wrench attack” – simply forcing the keys out of someone physically – became the defining risk, and CertiK noted that over half of France’s cases involved family members.

Key trends & patterns

AI is cutting both ways, and this quarter the defenders posted real numbers back: the IMF warned AI-enabled cyberattacks threaten financial stability, while Binance’s AI tools reportedly protected ~USD 10.5bn for about 2% of clients over 15 months, and the T3 unit froze >USD 450m worth of stablecoins. Regulation kept feeding the attackers’ target list – leaked taxpayer data is credited with fueling France’s kidnapping wave, and the French proposal to make residents declare larger private-wallet holdings could hand criminals another gift. But the numbers still favor attackers on the ground – physical violence remains the dominant threat vector, with France’s 41+ year-to-date sitting atop the 2025 escalation, plus a Swedish mock execution and a wave of kidnappings, pushing executive-security spending into the millions. The enforcement ledger kept filling in parallel: Celsius founder Alex Mashinsky’s lifetime crypto ban on top of his 12-year sentence, FTX founder Sam Bankman-Fried’s rejected appeal (25 years standing) and fresh pardon request, plus counterfeit-hardware and fake-app campaigns draining real money. The DeFi exploits sit here too, with the Drift theft (>USD 280m) and the Kelp DAO exploit (USD 292m). The quarter’s practical takeaway hasn’t changed: buy hardware wallets only from the manufacturer, never type seed words into any app, and don’t advertise what you hold.

What to watch in Q3

- How will jurisdictions respond to the growing trend of physical attacks, and will anti-privacy policies continue to feed criminals with new target lists?

- What new tools are emerging, such as the Gart app, to help protect Bitcoiners in the event of a physical attack?

- Do AI defense tools keep pace with AI-enabled attack methods, or fall behind?

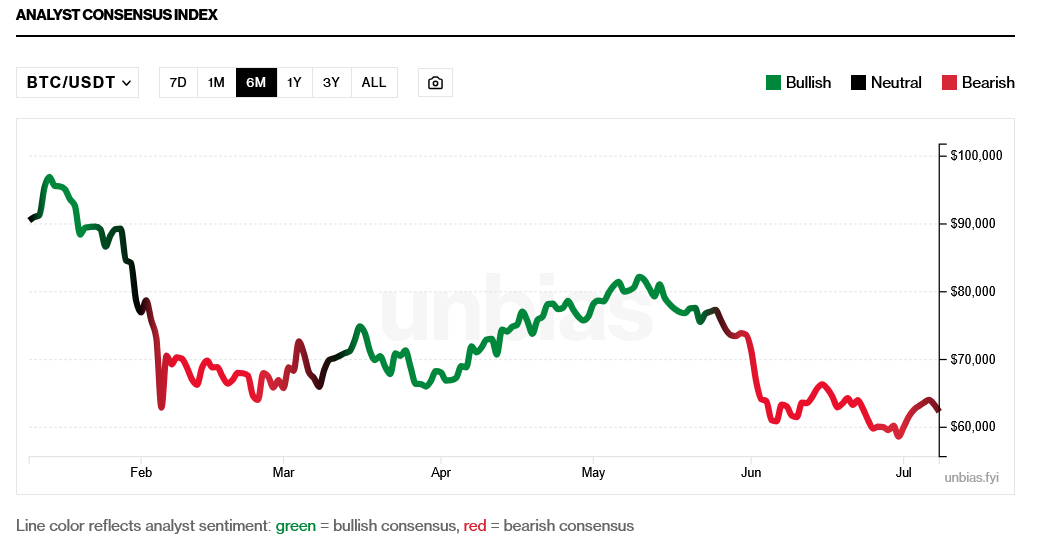

Market

The spring rally failed the test the market set for itself, the AI trade drained what demand remained, and bitcoin closed Q2 down 14% after nearly touching USD 58K – with the floor estimated anywhere between USD 40K (or lower) and "already in."

What drove Q2

Q2 compressed Q1's whole arc – hedged optimism curdling into bear-market confirmation – into thirteen weeks. April delivered +12%, the best month in a year, and a reclaim of USD 80K. The market then set its own verdict line: a May close above USD 76K would mark three straight up months and the end of crypto winter. May closed down 3%. By the market's own test, the bear phase resumed, and June supplied the proof – a slide to nearly USD 58K, the lowest since October 2024. Relative performance told the same story: April opened with bitcoin up 3% against gold's -9% monthly drop, reviving the overtaking-gold script; by late June the roles had reversed – gold down 9% on the month, bitcoin down 15%. Mid-May's optimism, from Tom Lee to derivatives traders flipping long, turned out to be the newsletter's standing rule in action: narratives follow price, not the other way around.

Two forces set the tempo. Iran was the quarter's metronome – war news drove April's whipsaws, and the late-June fragile peace signals produced the only durable bounce – while macro flipped from support to headwind: rate-cut hopes faded, oil and bond-market stress spilled into risk assets, and Jerome Powell's May exit installed a Fed chair, Kevin Warsh, whose first comments read inflation-first. Into that, the AI trade moved from threat to driver, while capital also rotated toward the SpaceX mega-IPO, and miners sold record amounts of bitcoin to fund their own AI pivots – one trade draining both sides of the market. June's break below USD 60K carried the longest causal stack of the quarter: equity rotation, USD 2.5bn of liquidated longs, lingering quantum-computing fears, and an overreaction to a 32-BTC sale by Strategy. ETH did worse, falling 25%, with Harvard selling its position outright.

Forecast dispersion, Q1's most telling data point, widened further: Bitfinex modeling USD 40K, chartists USD 48K, Standard Chartered declaring the USD 59K low already in, 21shares still holding USD 100K by year-end, and Bernstein being even more bullish – USD 150K by year-end. Meanwhile, Reza Bundy, Nouriel Roubini's partner, captured the state of modeling best with another -70% within six months, then USD 500K. Either way, nobody has a working model – but now the consensus is bearish, but here’s the trap: dominant expectations have been wrong on multiple occasions.

Q2's specific tension: leverage dropped and tourists left, holders didn't. ETF outflows ran every week of June, and treasury companies slowed, yet ETF holdings in BTC terms fell “only” 18% from October's highs against a 52% price drop, and the long-term-holder share kept rising. The selling is real, but the capitulation isn't – yet.

Underneath ran a liquidity drought: daily turnover shrank from USD 70bn+ during the early-June selloff to USD 24bn by late June, spot demand stayed thin, and derivatives steered the price – a market this shallow is one where a single unexplained event, like the USD 1.26bn one-day dump of BlackRock BTC ETF shares that nobody has claimed or explained, moves the tape.

And the quarter's most honest observation wasn't a price call at all: no analyst could answer the newsletter's standing question – why allocate to Bitcoin without believing its long-term case as a neutral global monetary network – and June's flows suggest institutions couldn't either. This and next year may mark a newly forming understanding of what Bitcoin and bitcoin are, with price implications nobody can time.

Fundamental positioning entering Q3

The regulatory hopes that propped up mid-May didn't deliver: the US market-structure bill ran out of road before July 4, leaving bank capital-requirement relief and the 401(k) proposal – the largest single demand-pipeline item – as carried-over wildcards, while MiCA's July 1 cutoff narrows the EU market to the licensed few. Market structure improved into a demand vacuum: CME futures and options went 24/7, killing the CME gap, and Morgan Stanley's lowest-fee ETF launched – better institutional rails, no institutional bid. Strategy, the market's dominant buyer, is now itself the stress point – STRC breaking from its price target, and BTC sale. Meanwhile, demand is mostly routing around bitcoin, while BTC is still mostly being held and borrowed against, while other use cases are lagging. One more thing carries into Q3: volatility is compressing, historically the setup for a large move – direction unknown.

Q3 scenarios to watch

Scenario 1: the floor test. If the USD 58–60K zone holds through the next macro shocks – the new Fed chair leans inflation-hawkish, the Iran conflict – and June's USD 1.3–1.8bn weekly ETF outflows moderate, Standard Chartered's "low is in" call gains ground; a decisive break opens the 48K and 40K models. The heavily short derivatives book is the accelerant: June 15 showed how fast liquidations flip direction. Price sits on the 200-week moving average – historically a zone returning over 100% within a year – but Q2's own theme is doubt that pre-2026 models still apply (however, the four-year cycle crowd is still alive); periodic buying remains the only strategy the commentary endorses regardless of direction.

Scenario 2: the Strategy checkpoint. STRC's twice-monthly dividends start in July. If the market keeps forcing the company to keep selling BTC, the dominant buyer becomes a supplier. Watch dividend payments, purchase announcements, and whether Capital B's authorized billions become actual buying.

Scenario 3: the autumn-recovery consensus. The market has penciled in an autumn bottom – the same market whose dominant expectations keep failing. Watch the channels that could actually deliver demand: bank BTC products going live, yield-bearing BTC products, capital rotating back after the IPO wave, and from the somewhat overhyped AI sector. However, these are predictable demand sources, and Bitcoin can always surprise. Let's hope it is a pleasant surprise.

This is what Dessenter sounds like in English.

A weekly English edition is launching soon — the same no-fluff Bitcoin and crypto intelligence that readers have been getting for years, saving them hours and bringing actionable information every week, now for a global audience. The weekly edition will be a paid publication with a 21-day free trial — sign up now to be first in line when it launches.

Note: You'll receive a confirmation email in Lithuanian — just click the button to confirm. Our English edition is coming soon.

Komentarai