Q1 in Bitcoin and Crypto: Key Trends, Patterns, and What to Watch in Q2

Hello!

Today is April 2, 2026, and it is the 4,770th day that Bitcoin has been operating 24/7 without any hiccups.

This is the Q1 2026 Quarterly Overview from Dessenter — the first one ever, built from months of weekly coverage in our Lithuanian newsletter, now distilled for a global audience. It's for investors, builders, and curious professionals who want to stay on top of Bitcoin and crypto without drowning in noise. If you don't have time to follow the market daily but don't want to miss what matters — this is your shortcut.

Each section opens with key trends and patterns, followed by opinionated analysis, and closes with what to watch in Q2. If you're short on time, the trends alone give you the quarter in under a minute. If you want depth, the analysis connects the dots that most summaries skip.

This overview covers roughly twenty categories — from regulation and stablecoins to AI agents, mining, DeFi, tokenisation, and beyond. It also marks Dessenter's first step into the global market. Expect these quarterly, and if you find it useful, subscribe below. It also marks Dessenter's first step into the global market — with a weekly English edition launching soon. Once launched, the first few weekly issues will be free for everyone.

Note: You'll receive a confirmation email in Lithuanian — just click the button to confirm. Our English edition is coming soon.

Author's analysis, AI-assisted drafting.

Regulation

Regulators worldwide raced to build frameworks for stablecoins and licensing while the US got stuck in an ugly fight over who profits from the rules.

Key trends & patterns

- Regulatory progress was real, but incumbents immediately shaped rules to protect their own revenue.

- The entire American crypto regulation debate collapsed into a fight over stablecoin yield.

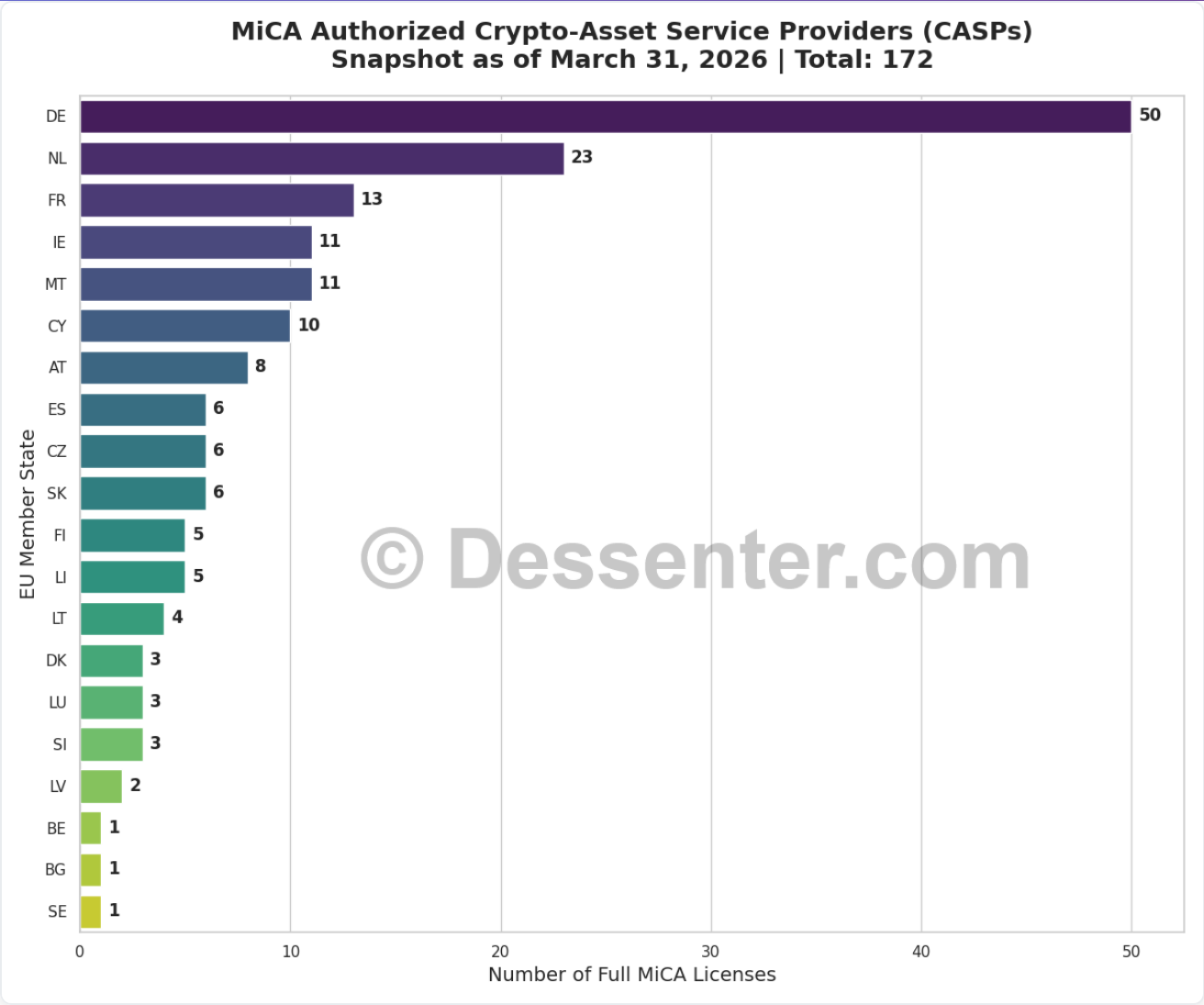

- 170+ MiCA licenses issued in total, while unrealized capital gains taxes and private wallet tracking are the next front.

- UK zigzagged as it ordered banks to stop blocking cryptoasset companies, then labeled it a growing fraud risk and banned political crypto donations, while regulatory consultations entered their final stage.

- EU Parliament rejected mass surveillance proposal, but the fight is not over; US acknowledged crypto mixers have legitimate uses.

- Basel capital requirements still punish banks for holding bitcoin — lobbying continued.

- In Russia, full crypto regulation planned for 2027, with banks potentially running exchanges — controlled liberalization, not freedom.

The quarter's dominant pattern was the usual play between regulatory progress (frameworks shipping, licenses issued) and lobbying (incumbents shaping rules to their needs). Nowhere was this clearer than in the US, where the stablecoin fight consumed all the oxygen. The OCC proposed banning yield on stablecoin holdings, Coinbase blocked the Clarity Act to protect its stablecoin revenue, and capital gains tax relief advanced for stablecoin payments — but not for bitcoin. The company was publicly accused of lobbying against bitcoin's interests; CEO Brian Armstrong went quiet when pressed. Trump, eyeing midterms, publicly sided with stablecoin yield, but his administration's actual legislative output stalled. The SEC did deliver one genuinely clarifying moment — its first formal classification of cryptoasset categories — though this formalized what the industry already assumed rather than breaking new ground.

In Europe, MiCA licensing passed 170 approvals and is now even more an operational reality, not a talking point. Germany, France, and the Netherlands lead. The more consequential EU development was less visible: the Netherlands moving toward a 36% tax on unrealized capital gains from 2028, and AMLA's mandate to identify private wallet owners above €1,000 by mid-2027. Circle pointed out that current EU rules block euro stablecoins from institutional settlement — a signal that the possible MiCA's first revision cycle is already being lobbied.

Russia continued its slow, controlled opening — planning full regulation from July 2027, floating the idea of banks running crypto exchanges without extra licenses — while the UK delivered a rare pro-crypto surprise by ordering banks to stop blocking crypto businesses, then immediately undercut the goodwill by labeling crypto a "growing fraud risk" and “temporarily” banning cryptoasset donations to political parties.

The Basel capital requirements for banks holding cryptoassets debate stayed alive but unresolved, with the Bitcoin Policy Institute lobbying as the committee itself hinted at softening already in 2025. PwC's annual assessment captured the quarter's real story: "regulation is no longer shaping crypto from the outside" as it "is being pulled into place by market reality."

What to watch in Q2

- US Clarity Act deadline. If the stablecoin regulation bill doesn't pass before summer recess, it might die for 2026. Watch whether Coinbase blinks on the yield question and whether Bitcoin advocates win against the stablecoin camp in the fight for the tax relief for everyday purchases.

- Emerging regulatory trends. While stablecoins captured most of the attention, tokenization, DeFi, and prediction markets are also rising on the regulatory radar.

- Privacy and surveillance. Fights over “Chat Control” and other initiatives such as plans to identify cryptoasset wallet owners on transactions above €1,000 or implement backdoors into hardware wallets, signal that regulators still opt for dangerous and largely inefficient surveillance and control practices.

- EU unrealized gains taxation. The Netherlands proposal seems to be off table for now, but if it returns in one form or another, it could be another worrying signal for other member states.

AI Agents

Everyone built payment pipes for AI agents — bitcoin, stablecoins, and card networks all shipped infrastructure — but actual transaction volumes stayed negligible, leaving the quarter defined by positioning rather than product-market fit.

Key trends & patterns

- Agent payment infrastructure shipped from every direction, but actual volumes stayed negligible.

- Transaction counts collapsed 97%, but average values jumped from cents to double digits.

- Corporate agents default to stablecoins/cards; autonomous agents gravitate to bitcoin/Lightning — no winner yet.

- Stablecoin nanopayment experiments might directly challenge Lightning's AI agent use case.

- No one established who's responsible when an autonomous agent with a wallet goes wrong.

- Agents hired humans, created child agents, bought goods — novel, but not yet systems.

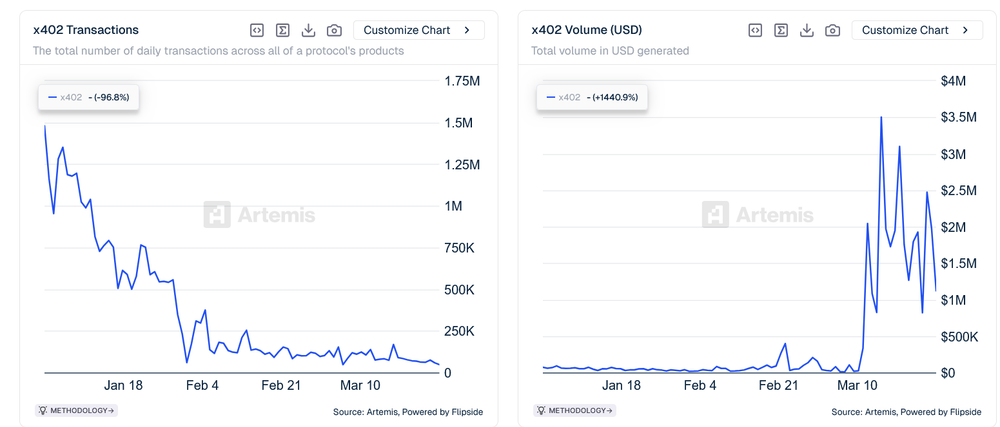

Q1's AI agent story was an infrastructure arms race with almost no customers yet. The numbers tell it plainly: Bloomberg's headline figure of ~$24M/month in agent crypto payments turned out to be closer to $1.6M on closer inspection, and the x402 protocol — the most visible non-bitcoin agent payment standard — saw transaction counts collapse from 1.5 million to 48,000 over the quarter. Yet average transaction values jumped from cents to $13–42, and the seller count doubled past 4,500. Seems like the market is shrinking in volume but growing in seriousness. This is textbook early infrastructure: the plumbing is being laid before the water flows.

The payment competition shaped up along predictable lines. Coinbase, Stripe, Tether, and MoonPay all shipped stablecoin-based agent wallets and payment tools. Stripe went furthest, launching its purpose-built Tempo blockchain. Visa and Mastercard entered with experimental tools and card-based agent payment solutions, joined by various startups. On the bitcoin side, Lightning Labs shipped new tools for bitcoin-preferring AI agents and the Bitcoiner argument — that Lightning is much cheaper than Ethereum L2 and settles in milliseconds — gained supporting data from a Bitcoin Policy Institute study showing 79% of agents chose bitcoin for asset protection, even though 53% defaulted to stablecoins for everyday transactions. Circle testing stablecoin "nanopayments" is a direct attack on Lightning's strongest claim: micropayment dominance. However, technically, Lightning still wins.

As I wrote earlier, the Agentic economy developing in three phases — chaotic experiments, multi-rail coexistence, then long-term bitcoin dominance — is a reasonable map but shouldn’t be mistaken for inevitability. The honest read is that corporate agents will likely settle on stablecoins and cards for compliance reasons, autonomous agents may gravitate to bitcoin for censorship resistance and freedom, while the boundary between these worlds is nowhere near defined. However, the AI-to-AI economy is likely to be much smaller than the AI-to-”real world” economy.

Beyond payments, the quarter produced genuinely novel moments. Meta acquired agent social network Moltbook (200K agents), likely bringing payments into its ecosystem. Rentahuman.ai is nearing 700,000 registered humans ready to be hired by AI agents for real-world tasks. One agent created a "child" agent and used bitcoin to buy it data access. These are still stunts more than systems — but the pattern of agents autonomously managing money is no longer hypothetical.

The unsolved problems are piling up as fast as the products. Electric Capital flagged the legal liability vacuum — who's responsible when an agent with a wallet goes wrong? — and Q1 provided a live example when an agent accidentally transferred hundreds of thousands. Mastercard and Google built verification tools, MoonPay and Ledger built authorization systems, and Sam Altman's World partnered with Coinbase on identity. None of these is a standard yet. The identity and authorization layer seems to be the real bottleneck, not the payment rails.

What to watch in Q2

- Actual payment volumes, not infrastructure announcements. Q1 was all supply, and relatively no demand. The first protocol to show sustained, growing transaction counts — not just rising average values — will have the strongest signal. Watch x402 metrics specifically. BTC payments over Lightning are difficult to track, but the industry still might provide estimates.

- Meta + Moltbook integration. If Meta connects payments to hundreds of thousands of agents inside its ecosystem, it could instantly become the largest agent economy by user count — and the payment method it chooses (stablecoins, likely) would set a powerful default. However, the agentic economy is not on a firm ground yet, as AI giants, such as Claude, might make agents obsolete in many cases.

- Circle nanopayments moving from testnet to production. If stablecoin micropayments become cheap enough to rival Lightning, bitcoin's advantage in agent-to-agent transactions narrows significantly. However, stablecoins can still be frozen in your wallet.

- Legal liability clarity. Any regulatory guidance on who bears responsibility for autonomous agent financial activity would substantially shape the entire competitive landscape.

Adoption

Besides payments, which are analyzed in a separate section, bitcoin and crypto usage kept expanding across institutions, crisis zones, and new financial products, even as prices halved — proving that adoption has decoupled from the market cycle.

Key trends & patterns

- Price fell nearly 50% from highs while real-world usage metrics — users, merchants, bank products — kept growing steadily.

- Institutional cryptoasset allocation intent hit multi-year highs even as market prices declined through the quarter.

- Sovereign and pension-scale capital began exploring direct cryptoasset exposure, signaling demand from a new buyer tier.

- Russia built a parallel cryptoasset financial layer at the bank level, expanding lending, derivatives, and asset services.

- Cryptoassets proved their utility as crisis money in active conflict zones where traditional financial infrastructure collapsed.

- Cryptoasset-backed real estate and mortgage products emerged as a new frontier for collateralizing illiquid holdings.

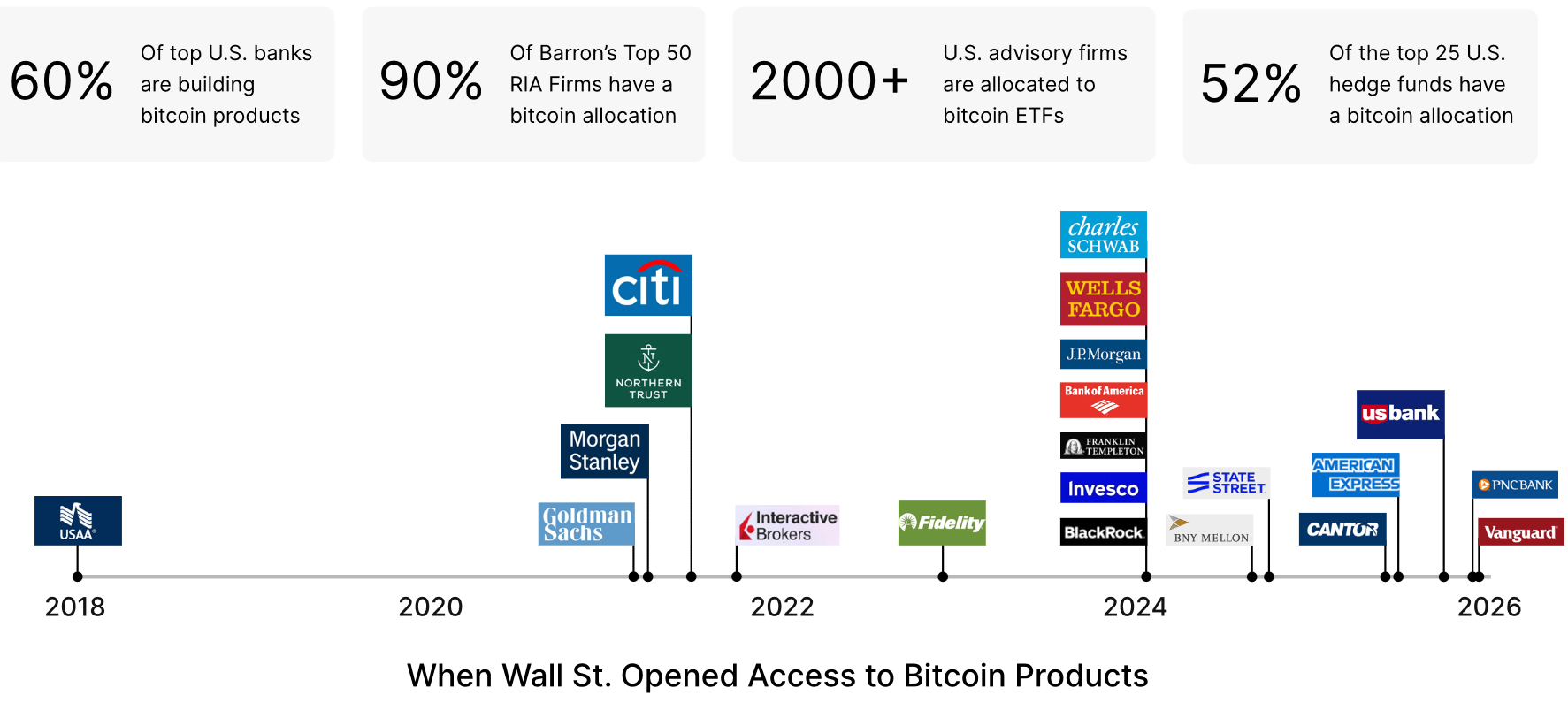

The most striking pattern of Q1 was the growing gap between price action and real-world usage. Bitcoin's price fell almost 50% from its highs, yet Tether data showed the network adding 10 million users per quarter, reaching 571 million, while River documented that US businesses accepting bitcoin tripled and 60% of the largest US banks were actively building bitcoin products.

Institutional conviction deepened despite the downturn. The Coinbase/EY-Parthenon survey of 351 institutional investors in January found 73% planning to increase crypto allocations in 2026, with 86% interested in stablecoins. Kazakhstan's central bank committed USD 350 million to digital assets. Australia's Hostplus pension fund (AUD 150 billion) began exploring crypto for its 2.2 million members. At the same time, the U.S. Department of Labor proposed a rule that would allow 401(k) managers to offer their clients cryptoasset-related funds while also providing better protection. Meanwhile, the New Hampshire Business Finance Authority might issue possibly the first rated (by Moody's) BTC-backed bond. The CfC St. Moritz survey of 242 market participants in January confirmed improving macro sentiment and declining regulatory risk perception — with fintechs and tokenization named the most exciting sectors.

Russia quietly assembled a parallel crypto-financial layer. Sberbank and Sovcombank both launched cryptoasset-backed lending, Moscow Exchange added cryptoasset derivatives, and the regulatory trajectory pointed toward broader bank-level cryptoasset services — even as the country's largest Bitcoin miner BitRiver faced bankruptcy.

Iran provided the starkest demonstration of cryptoasset's utility as crisis money. Citizens used cryptoasset to protect their savings as the local currency collapsed and traditional financial infrastructure failed during the military conflict. The country is accepting crypto payments for weapons, while limited-internet workarounds — mesh networks, satellite, Opendime — kept being tested in the field not only in Iran.

New financial products expanded cryptoasset's practical reach. Coinbase and Fannie Mae began developing cryptoasset-backed mortgages in the US. In Europe, Brighty said they facilitated over 100 real estate transactions using cryptoassets (USD 500K–2.5M each). Multicoin Capital outlined a thesis that the next adoption wave will come through earning, not buying — people entering crypto by providing data services and labor, not by purchasing tokens. Japan's Bitcoin giant Metaplanet took this infrastructure-first logic further by creating a new division to invest approximately USD 27 million into domestic Bitcoin companies spanning custody, lending, payments, and stablecoins.

Meanwhile, a16z forecast that prediction markets, SNARK technology expanding beyond blockchains, and "staked media" — a model where content creators put money behind their claims — would be among the year's most significant developments.

What to watch in Q2

- “Bitcoin identity” changes. How the so-called “Bitcoin identity crisis” will evolve in the mainstream audience and what next narrative might form.

- Real flows. Whether institutional allocation surveys translate into actual capital flows, particularly from pension funds and central banks that signaled interest in Q1.

- Bank moves. Watch for more European banks applying for MiCA licences, as bitcoin/crypto sectors keep merging.

- Safe haven narrative. Whether Bitcoin and other cryptonetworks strengthen their image as alternative system, serving as a hedge from traditional systems problems.

Stablecoins

Stablecoins stopped being a crypto subsector and became a battlefield where payment incumbents, banks, regulators, and geopolitical interests are fighting over the future architecture of money, which still resembles more the traditional fiat system rather than true innovation.

Note: While stablecoins are a part of the broader payments landscape, the sheer volume of Q1 developments — from billion-dollar M&A to sovereign risk warnings to new issuer proliferation — warrants a dedicated category.

Key trends & patterns

- Traditional finance shifted from watching stablecoins to actively building and issuing them.

- Payment giants spent billions acquiring stablecoin infrastructure, consolidating the rails.

- Only 7% of stablecoin volume goes to real commerce.

- Europe's licensed stablecoin ecosystem expanded, with euro stablecoins dominating the non-dollar market.

- The yield debate — whether stablecoins can pay interest — stalled US legislation.

- Centralized freezing of over USD 2 billion in total exposed the permissionless-payments contradiction.

- Sanctions evasion and digital dollarization turned stablecoins into a geopolitical flashpoint.

- Bitcoin-native stablecoins emerged as a distinct new design direction.

The defining shift in Q1 wasn't stablecoin growth — that was already underway — but the speed at which traditional finance moved from observation to construction. Fidelity launched its own stablecoin, PayPal expanded PYUSD from 2 countries to 70, Meta began exploring third-party stablecoin payments. On the infrastructure side, Mastercard paid USD 1.8 billion for BVNK, while Visa and Stripe/Bridge announced stablecoin card expansion to over 100 countries, and Stripe" was reportedly considering acquiring PayPal. The competitive pressure was already visible: Block fired 40% of its workforce, with analysts linking the cuts partly to stablecoin margin compression, besides the impact of AI.

The data revealed a paradox: stablecoins are clearly eating into traditional payments, but real commerce use remains a sliver. Only 7% of the USD 62 trillion total stablecoin volume goes to goods-and-services payments. B2B payments grew 773%, card payments 673% in 2025 — explosive rates off a small base. The IMF estimated stablecoins reduce payment incumbents' value by 18%, while Standard Chartered forecast a USD 2 trillion stablecoin market by 2028 and warned US banks could lose USD 500 billion in deposits. However, the bank also emphasized recently that stablecoin velocity, or a measure of how fast tokens are moving through the systems, has increased which might reduce the need for new issuance of stablecoins. For now, the bank doesn’t change its 2028 forecast.

Another possible paradox is that Visa and Mastercard executives publicly dismissed stablecoins as unnecessary for developed-market payments — while their companies assembled massive partner coalitions and acquired stablecoin infrastructure for billions. While it might mean they plan to focus on less-developed market, it might also show the gap between messaging and action.

Two structural tensions sharpened. First, the yield war: the US Clarity Act stalled because Coinbase refused to accept a ban on stablecoin interest payments. Whether stablecoins compete with banks as savings vehicles or stay confined to payments remains unresolved. Second, censorship risk crystallized — over USD 2 billion in frozen wallets exposed the contradiction between permissionless branding and centralized control as businesses are being left without access to their money.

Geopolitically, stablecoins became a two-sided weapon. Russia's sanctions-evading ruble stablecoin A7A5 surged to USD 90 billion in market cap, while the FSB warned that dollar stablecoins could trigger digital dollarization in weaker-currency countries. Meanwhile, Bitcoin-native stablecoins began emerging as a distinct trend, with multiple projects launching on Bitcoin L2s and the Bitcoin base layer — potentially reshaping Bitcoin's role in the stablecoin market.

What to watch in Q2

- The Clarity Act. Whether the stablecoin interest ban survives or falls will define the competitive landscape between crypto firms and US banks for years.

- Euro stablecoin launch by the Qivalis banking consortium. It's planned for H2 2026 — the first multiple banks-backed euro stablecoin could reshape European stablecoin dynamics.

- Stripe/PayPal acquisition rumors. Confirmation or denial will signal how aggressively fintech consolidation around stablecoins proceeds.

- Bitcoin-native stablecoins. Whether stablecoins on Lightning and Ark protocols gain traction or remain niche experiments.

Payments

Bitcoin payments infrastructure crossed a critical threshold — from opt-in curiosity to default-on for millions of merchants — while the data increasingly showed that real commerce, not speculation, is driving payment adoption.

Note: Stablecoins have become the key player in the payments industry, but the scale of Q1 developments warrants their own dedicated section. This analysis focuses on bitcoin, Lightning Network, crypto card payments, and the broader non-stablecoin payments infrastructure.

Key trends & patterns

- Default-on bitcoin acceptance at a major POS provider is more important than any opt-in campaign ever was.

- Lightning Network is outgrowing micropayments — processing billions annually, with single transfers hitting USD 1 million.

- Merchant adoption data from multiple sources consistently shows crypto payments growing, not plateauing.

- Grassroots payment tools are multiplying across regions, lowering the barrier to accepting bitcoin to near zero.

- Crypto card payments grew 15x in two years, opening a familiar spending channel for crypto holders.

The quarter's payments story has a clear headline: infrastructure is catching up with demand. Square flipping Lightning payments to default-on for its 4 million US merchants was the single most consequential event — it shifted bitcoin acceptance from opt-in to opt-out, a fundamentally different adoption dynamic. More acceptance points are the strongest driver of payment adoption, and this move delivered them at scale overnight.

Lightning Network matured visibly. According to River estimations, the network processed over USD 1.7 billion in November 2025 alone, with payment value up 300% year-on-year. However, the number of transactions dropped, showing that Lightning is now increasingly used for larger transactions. The first known USD 1 million Lightning transfer shaped the micropayments-only narrative too. An infrastructure developer estimated annual Lightning throughput now exceeds USD 10 billion, though the figure is speculative given the network's privacy properties.

Lithuania's CoinGate also offered a grounding data point — payment volumes dipped 15% due to structural factors, not demand, while BTC used the situation to reclaim the top spot as the most-used payment method, overtaking stablecoins.

Merchant evidence reinforced the trend from multiple angles. US businesses accepting bitcoin tripled in 2025, small businesses led adoption, and a merchant survey showed 88% of respondents saying customers actively ask about crypto options. One fast-food chain reported a 15% sales bump on some of its restaurants after enabling bitcoin payments. Grassroots tools — from Thailand's fiat-conversion QR codes to tap-to-pay NFC solutions to decentralized Nostr marketplaces — kept lowering the floor for acceptance. Crypto card payments grew from USD 100 million in 2023 to over USD 1.5 billion in 2025, turning a negligible channel into a real one.

A structural counterweight: the Bank for International Settlements warned that blockchain proliferation fragments the market and weakens the network effects payments depend on. Too many competing rails could slow the very adoption all these tools are chasing.

What to watch in Q2

- Square default-on impact data. We might see the first real metrics on what happens when 4 million merchants have bitcoin payments enabled by default and whether bitcoin payments can compete with stablecoins in a developed economy.

- Crypto competition. How will WalletConnect’s partnership with payments giant Ingenico affect the expansion of crypto payments, increasing competition for bitcoin further.

- Lightning expansion. Whether Lightning Network's shift toward larger transactions continues to attract institutional and commercial users, or hits scaling friction.

- New protocols. How will the emerging Ark Protocol-powered solutions affect bitcoin payments.

- Tax relief. The battle over the capital gain tax relief for bitcoin everyday purchases in the US, which might unlock a new wave of adoption.

- Institutional partnerships. Mastercard 85+ partner coalition and Visa Direct stablecoin integration — whether these translate into actual merchant-facing products or remain press-release partnerships.

- Grassroots tools. Watch whether tools like PlebQR, Numo, and Cashu protocol-based solutions — whether they gain traction beyond early-adopter communities in specific regions.

Wallets

Bitcoin and crypto wallets evolved from passive storage devices into active financial platforms — bridging traditional banking, Lightning payments, and yield products — while the tension between self-custody and regulatory pressure intensified.

Key trends & patterns

- Wallets are shifting from selling devices to earning revenue from active user transactions and financial operations.

- Hardware wallets became payment tools, not just storage — first devices now support instant, cheap, and private bitcoin transactions.

- European startups are bridging traditional bank accounts and Bitcoin wallets with automatic euro-to-bitcoin conversion.

- Wall Street banks are entering the wallet market, but cryptoasset-native UX and security standards remain hard to match.

- Next-generation Bitcoin wallets aim to unify multiple protocols into one interface, hiding technical complexity from users.

- Regulatory pressure is pushing wallets away from custodial models in Europe, forcing self-custody on users, ready or not.

- Privacy tools and blockchain surveillance remain locked in an escalating arms race at the wallet level.

The wallet graduated from storage device to active financial tool. Hardware wallets gained Lightning Network support, making them capable of both cold storage and real-time payments. Software wallets added multi-protocol stacks combining Lightning, privacy features, and altcoin support. Revenue confirmed the shift: wallet makers are now generating millions in monthly fees, and one hardware manufacturer doubled its annual revenue — not by selling more devices, but because existing users started transacting more.

A distinctly Baltic/European category emerged: IBAN-to-bitcoin bridge wallets. Bitcoin teams such as Bringin and Wave.space launched products that tie a euro bank account directly to a bitcoin wallet, automatically converting between the two. This targets a specific, practical gap — letting users move between traditional banking and self-custody without manual steps or intermediary platforms.

Traditional finance entered the wallet space directly. A major Wall Street bank Morgan Stanley announced plans for a cryptoasset wallet, while the leading Ethereum wallet Metamask began offering tokenized stocks, blurring the line between wallet and brokerage. Not every entrant cleared the bar — one high-profile launch by Rumble and Tether drew immediate criticism for fees and security gaps, proving the UX and security standards are genuinely demanding.

Next-generation bitcoin wallet projects advanced meaningfully. Teams demonstrated wallets that unify Lightning, Ark, Liquid, and other Bitcoin layers into a single interface, abstracting protocol complexity from the user. The shared thesis: the future wallet routes transactions across layers automatically, and the user never needs to know which protocol handled it.

Self-custody came under pressure from two directions. Regulatory proposals threatened to mandate recovery mechanisms — fundamentally undermining non-custodial design — while a popular Lightning wallet, Wallet of Satoshi, dropped custodial services in the EU entirely, forcing users into self-custody. Meanwhile, privacy tools such as Payjoin ran into the persistent problem of wallet fingerprinting: even enhanced transactions can, in theory, be traced through wallet-specific digital signatures. Countermeasures are in development, but the surveillance arms race continues.

Security remained a weak link, with yet another client data leak at a major hardware wallet maker Ledger — this time through a partner — reinforcing that third-party data sharing or collecting user data at all remains a risk even for security-focused companies.

What to watch in Q2

- New hardware wallet features. Look for new partnerships, integrations, and features that could make your online or hardware wallet more than a passive tool to store and transact with bitcoin.

- On-ramp/off-ramp improvements. New solutions that would make bitcoin on-ramp/off-ramp even simpler.

- New entrants. Watch for launches and adoption news from Ark Labs, Bark, and Spark teams, developing Ark Protocol-powered solutions, which both complement and compete with Lightning.

- Non-custodial wallet regulation. How will no-KYC wallets evolve, giving users more breathing space from, and whether regulators will increase pressure on cryptoasset self-custody?

- Morgan Stanley wallet. Any concrete details on what it will actually offer and how it compares to crypto-native solutions.

- Expanding niches. While still a niche example, Cashu protocol can find interesting use cases both in bitcoin wallets and decentralized apps such as Bitchat.

Privacy

Developers shipped more privacy tools than ever, but Q1 revealed that building them is only half the battle — wallet fingerprinting, regulatory pressure, and a wave of physical attacks showed the gap between privacy as a feature and privacy as a lived reality.

Key trends & patterns

- Bitcoin's privacy toolkit grew, but a late-quarter fingerprinting discovery showed that protocol-level privacy means little if wallet software leaks metadata.

- Selective, toggleable privacy emerged as the pragmatic design pattern bridging cypherpunk ideals and institutional compliance needs.

- Physical attacks and major data breaches made the strongest case for privacy — not theory, but stolen funds and extorted users.

- The EU split: mass surveillance proposals rejected twice, but new rules targeting self-custody wallet identification are still being drafted.

- The regulatory attempts are increasingly reminding of the wack-a-mole game, as attempts to curb privacy are fought back with new technological solutions.

The quarter's privacy story played out on three fronts simultaneously: technical progress, real-world urgency, and regulatory tug-of-war.

On the technical side, Bitcoin's privacy stack advanced meaningfully. Payjoin — considered superior to Coinjoin because analytics firms cannot distinguish it from a normal transaction — gained adoption through Bull Bitcoin and Cake Wallet, which also integrated Silent Payments and added zcash support. Bitcoin Core v31 promised better transaction privacy for node operators. And Starknet introduced a wrapped bitcoin token with toggleable privacy, letting users choose between transparent and shielded modes. But the quarter's sobering technical discovery came in late March: researchers found that wallet-specific digital fingerprints can undermine Payjoin by allowing analysts to trace users through the metadata their wallet software leaves behind. A fix is already in development, but it was a reminder that privacy is an arms race, not a destination.

The urgency case made itself. Physical attacks on crypto holders intensified — France alone produced multiple incidents, including an attempted robbery of a Binance executive and a home invasion netting over USD 1 million in bitcoin. The CarGurus breach exposed 12.4 million user records, while a former Revolut employee's extortion case illustrated how centralized data collection creates targets. Binance’s Changpeng Zhao called privacy one of the key barriers to cryptoasset payments going mainstream — a notable statement from someone running a platform built on KYC that delisted privacy coin monero but still keeps zcash, which is considered to be more regulatory-compliant.

Meanwhile, a design pattern crystallized: selective, compliance-compatible privacy. Solana Foundation published a report positioning its chain for institutional-grade private transactions, alongside EY offering Nightfall on Ethereum. This institutional angle is significant as it reframes privacy from a cypherpunk demand into a business requirement.

The regulatory picture in the EU split down the middle. The European Parliament rejected Chat Control mass surveillance twice — a genuine win for digital privacy. But the EU's anti-money-laundering authority AMLA is still tasked with drafting rules to identify self-custody wallet holders making transactions above EUR 1,000 by July 2027, directly endangering bitcoin and crypto users. Dubai went further, banning privacy cryptocurrency trading outright. The dedicated Zcash ecosystem at least temporarily weakened after its developer split, though a new Zcash development company ZODL raised millions.

The privacy infrastructure proved stubbornly resilient. A Cambridge University study confirmed what many suspected: sanctions against crypto mixers don't work as intended — users simply migrate to new platforms.

What to watch in Q2

- Privacy-friendly wallets. Watch for wallets adopting Payjoin and/or Silent Payments, that increase your bitcoin privacy considerably. However, keep in mind, developers are still working to fix the wallet fingerprint problem for Payjoin payments.

- Regulatory attacks. Whether regulators will try to introduce new measures that would track and endanger bitcoin and crypto users, such as backdoors in hardware wallets.

- EU surveillance steps. While the AMLA’s July 2027 deadline is distant, the consultation process and early drafts might start appearing soon.

- Bitcoin Core v31 release. The spring update should make improved transaction privacy practically usable for node operators.

- Institutional offerings. Watch for new tools for institutional blockchain users and how it affects institutional blockchain/cryptoasset adoption.

Blockchains

Both Bitcoin and Ethereum spent Q1 searching for what they want to be when they grow up — Bitcoin torn between monetary purity and platform ambitions, Ethereum pivoting from "do everything" to "do what matters" — while developer talent bled toward AI, and mining centralization flashed a real warning sign.

Key trends & patterns

- Bitcoin's censorship-vs-openness war produced organizational splintering, not resolution — and cost a key developer.

- Bitcoin's L2 and application layer quietly thickened with multiple live launches.

- Ethereum pivoted from "do everything" toward focused data storage and consolidation under a new roadmap.

- Ethereum's L2 fragmentation became serious enough for both its own developers and the BIS to flag it.

- New security research exposed vulnerabilities in both Bitcoin infrastructure and Ethereum's latest upgrade.

- Mining centralization reminded us that this problem hasn’t been solved yet.

- Developer talent is bleeding from crypto to AI at alarming rates.

- Bitcoin crossed the 20 million supply milestone, with the final million stretching over a century.

Bitcoin's philosophical split continued all quarter. The BIP-110 debate over restricting non-financial blockchain data went nowhere, for now, failing to gain wider support. Even some previous supporters peeled off after, e.g., critics showed it would make Bitcoin wallets less secure. But the tension produced real consequences: Bitcoin Core maintainer Gloria Zhao left this position after six years, caught between warring camps, and the ProductionReady initiative launched with ambitions to create a "conservative" alternative node software. While it would be a fork of the most popular Bitcoin implementation, Bitcoin Core, this new software for running the network’s node would be less-friendly to Bitcoin’s non-financial transactions, such as NFTs.

Meanwhile, Bitcoin's L2 ecosystem kept building and shipping. Citrea launched its mainnet and established a development foundation. Ark Labs attracted Tether investment, Arkade Assets went live for stablecoins on Bitcoin, Polar launched AI-powered Lightning node management, and BitVM's Binohash proposed covenants without protocol changes. Individually incremental, collectively these are making Bitcoin's application layer substantially thicker.

Ethereum had its own identity rethink. Vitalik Buterin's positions evolved visibly — from "trilemma solved" in January, to attacking redundant chains in February, to proposing Ethereum as a "bulletin board" for storing important data rather than trying to be everything. The Ethereum Foundation reinforced this with a published mandate, a roadmap through 2029, AI trust layer ambitions, and a leadership handover. But the fragmentation problem — too many L2s, disjointed experience — grew serious enough to prompt the Ethereum Economic Zone proposal. Even the BIS flagged the fragmentation. Meanwhile, The DAO revival (ETH 70,500 (USD 150 million) toward security) and Vitalik's personal ETH 16,384 commitment showed consolidation, not expansion, is the mode. At the same time, Base, a Coinbase-developed Ethereum’s layer 2 blockchain turns its focus on stablecoins, tokenized assets, while trying to lure more developers and accommodate institutions.

Security got a reality check. OtterSec warned about ZK-VM-related bugs in various applications. Research found Bitcoin resilient to submarine cable disruptions but vulnerable to coordinated hosting company attacks. Ethereum's Fusaka upgrade cheapened "address poisoning" spam. An Italian central bank economist warned Ethereum could threaten financial stability.

Two structural concerns flashed. Mining centralization: Foundry at ~33% hashrate found 7 consecutive blocks amid a rare Bitcoin block reorganization, triggering debate on how many confirmations is now enough to be sure your transaction will not be rejected. Developer drain: crypto developer activity dropped ~75% since early 2025, active developers down 56% — pulled toward AI.

Bitcoin crossed 20 million BTC mined — 95%+ of supply, the rest taking ~114 years. On the margins: Robinhood launched its own chain, Allium moved 65 TB from 80+ blockchains data onto decentralized storage, and Chainalysis automated its surveillance toolkit.

What to watch in Q2

- BIP-110 deadline pressure. The proposal needs 55% miner support by September 1. With no mining pool backing yet (aside from the conflicted Ocean), Q2 will reveal whether this quietly dies or escalates further.

- Bitcoin L2 traction vs. skepticism. Citrea and Arkade Assets are all live. The question is whether real usage follows, or whether these remain infrastructure waiting for users — and whether the backlash against Bitcoin evolving into something bigger than money only intensifies.

- Ethereum's consolidation execution. The Ethereum Economic Zone, the Strawmap roadmap, and the AI trust layer positioning are all plans. Q2 will bring more evidence what Ethereum can actually deliver on simplification, or whether fragmentation keeps winning.

- Competition among blockchains. Watch how will competition evolve among blockchain, racing for the bigger share in the Agentic economy and Stablecoin pies.

- Bitcoin mining centralization. Whether the industry will react with more specific steps towards Bitcoin mining decentralization, or the Foundry “incident" will be quickly forgotten.

Quantum Computing

Bitcoin-friendly Wall Street players spent Q1 trying to calm the quantum fears it helped create, while developers accelerated technical preparations — but the quarter ended with Google research that may have just compressed the timeline everyone was banking on.

Key trends & patterns

- Google research on Q1's final day compressed perceived attack timelines and showed that Ethereum is more vulnerable than Bitcoin.

- Developers on both major blockchains accelerated practical quantum-defense work, moving from theory to testable code. However, it seems that Ethereum is winning this activity race.

- Post-quantum cryptography solutions are not the real problem — the real bottleneck is Bitcoin's slow, consensus-driven governance process.

- The debate over what happens to quantum-vulnerable coins is becoming a political question with no clean answers.

- Large institutional holders may disproportionately influence which quantum solutions get adopted, and when.

- Whether a cryptographically relevant quantum computer can exist at all remains genuinely unknown.

The quantum computing narrative in crypto underwent a visible shift this quarter: from background anxiety to organized institutional response. The pattern was unmistakable — Bitcoin-friendly Wall Street players lined up to publish reassurance reports. ARK Invest and Galaxy Digital both released analyses concluding that the quantum threat to Bitcoin is real but far from imminent, with Galaxy Digital CEO Mike Novogratz explicitly framing it as something Bitcoin will solve in time. The subtext mattered more than the conclusions: these reports were aimed squarely at institutional investors who possibly had pulled back from Bitcoin in 2025 partly over quantum fears.

On the technical side, progress was real. BIP 360 — the most prominent proposal for quantum-resistant Bitcoin transactions — was formally added to the BIP process, a meaningful procedural step. Ethereum Foundation moved and communicated more actively: it established a Post Quantum team, Vitalik Buterin presented a defense plan with a $1 million bounty for quantum-safe cryptography, and later consolidated all efforts under pq.ethereum.org. Strategy announced a Bitcoin Security program, while Coinbase set up an independent quantum advisory board with no bitcoiners included. Google set 2029 as its internal deadline for post-quantum migration of its authentication services.

Yet a critical tension runs beneath the technical progress. We still do not know whether a cryptographically relevant quantum computer can exist at all, or when it might emerge — estimated timelines range from several years to decades. Post-quantum signature schemes already exist. The hard part is not cryptography — it is governance. Bitcoin's decentralized upgrade process, built on the BIP system and voluntary consensus, is notoriously slow. Chaincode Labs has recommended a 2-year contingency plan and a 7-year comprehensive plan. A post-quantum migration would require coordinated wallet-level changes across millions of users. Some developers argue this may ultimately require a hard fork — a contentious prospect for any Bitcoin upgrade.

This governance question carries a politically uncomfortable corollary. Part of the community is already debating what happens to vulnerable coins — including potentially Satoshi Nakamoto's estimated million-plus bitcoin — and whether large holders like Strategy or BlackRock might disproportionately influence which solutions get adopted, and when. The "burn or steal" dilemma for quantum-vulnerable coins remains unresolved: do you let them be taken by whoever builds the first quantum computer, or do you impose protocol-level restrictions that contradict Bitcoin's property guarantees? Even proposed middle grounds, like the Hourglass mechanism for slowing vulnerable coin movement, spark fierce disagreement. Technical solutions are emerging, but the Bitcoin community faces a political question that might hurt BTC holders either way.

Then, on the last day of Q1, Google Quantum AI published research that may force developers to think and act faster. The team's findings suggest that breaking Bitcoin's and other blockchains’ cryptography could require less resources than thought. However, the research showed that Ethereum has a wider attack surface, vulnerable to quantum attacks. In either case, the immediate practical risk remains zero — no such machine exists. But the research compresses the perceived timeline and expands the scope of exposure, possibly undermining the "decades away" framing that is still popular among many.

What to watch in Q2

- Market and developer reaction to Google's quantum research. Whether institutional investors treat this as a meaningful risk reassessment or dismiss it as theoretical might shape BTC sentiment near-term.

- BIP 360 progress and governance debates. Whether the proposal advances toward serious review or stalls in committee-style disagreements will signal how fast Bitcoin can actually move.

- The political question of vulnerable coins. As quantum timelines compress, the debate over what to do with exposed bitcoin will intensify. This is where governance meets property rights — and where the community's response could define Bitcoin's credibility with institutional capital.

- Ethereum's centralization and communication advantage. With pq.ethereum.org and a centralized coordination effort, Ethereum is setting the pace on quantum messaging. Whether Bitcoin can match this without a comparable organizational structure remains an open question.

Like what you're reading? A weekly English edition is launching soon — free for the first 21 days. Get notified:

Note: You'll receive a confirmation email in Lithuanian — just click the button to confirm. Our English edition is coming soon.

Companies

Crypto companies spent Q1 caught between two forces — traditional finance accelerating its entry and a bear market forcing layoffs, IPO delays, and closures — while Tether built an empire and bitcoin reserve companies absorbed billions in paper losses.

Key trends & patterns

- Traditional banks moved from crypto curiosity to crypto execution — licensing, trading, custody, and stablecoin integration all at once.

- Crypto entered insurance and mortgages — BTC-linked products and crypto-aware loan assessments are now real.

- The bear market triggered an industry-wide layoff wave and forced multiple IPO delays or freezes.

- Some crypto firms shut down despite strong usage metrics — the market punished those without sustainable economics.

- Bitcoin reserve companies absorbed billions in paper losses, forcing a rethink of the treasury-only model.

- Tether had its most consequential quarter ever — aggressive investments, US re-entry, and Big Four auditor engagement.

- Venture capital stayed active but selective — multiple new unicorns, but funding concentrated in infrastructure and compliance.

- Financial results split sharply: fintechs with diversified revenue thrived, pure-crypto plays bled.

- Stock exchanges and traditional platforms began building tokenized securities infrastructure in earnest.

- X Money launch announcement left crypto integration as the quarter's biggest unresolved corporate question.

Key trends & patterns

The volume of traditional financial institutions moving from exploration to execution defined Q1. Morgan Stanley confirmed bitcoin custody and lending plans. UBS opened crypto trading for select clients. DZ Bank got a MiCA license. Danske Bank enabled exchange-traded BTC/ETH products. Interactive Brokers launched cryptoasset trading for retail investors in the European Economic Area. Wells Fargo registered a crypto mark. The New York Stock Exchange started building a 24/7 tokenized securities platform, Nasdaq partnered with Seturion for tokenized equities, and EY warned that businesses need crypto wallets alongside bank accounts. Even insurance (Delaware Life) and mortgages (Newrez) joined in. Meanwhile, Sharon AI borrowed USD 500 million via blockchain lending for GPU infrastructure, showing crypto rails extending beyond crypto-native firms.

But this ran into a bear market and AI. Layoffs hit Gemini (-30%), Block (-40%), Crypto.com (-12%), Algorand Foundation (-25%). IPOs stalled — Kraken froze, OKX delayed — while Tally, Balancer Labs, and WebN shut down entirely. Nakamoto, shares down 98%, scrambled to survive through internal acquisitions. However, BitGo successfully completed its IPO in January.

Reserve companies took massive hits. Strategy posted a USD 12.4 billion Q4 loss; Bitmine USD 8.4 billion. The model itself was questioned: Steak 'n Shake — accepting BTC, building reserves, paying staff in bitcoin atop a real business — emerged as the template, against pure treasury plays that were failing. For example, in March, hyped BTC treasury firm Nakamoto sold BTC for USD 20 million at a 40% loss to fund its operations.

Tether had the most consequential quarter of any single company: USD 10 billion annual profit, investments spanning Gold.com, Anchorage, Whop, and others, US re-entry with USAT, and — most significantly — KPMG and PwC (which expanded crypto services early in Q1) engagement, ending years of limited BDO Italia attestations.

Venture capital stayed selective. Dragonfly (USD 650 million), Ledn (USD 188 million), Mesh and TRM Labs (both reaching unicorn status) stood out. New funds from a16z crypto, Paradigm, and Haun Ventures were in preparation. Financial results split sharply: Revolut (+57% profit, UK bank license) and Coinbase (USD 1.78 billion Q4 revenue) showed strength, while Fold, Bitpanda, Exodus, and Bullish posted losses despite growing usage. Ripple hit a USD 50 billion valuation; CoinGecko was reportedly for sale at USD 500 million.

Elon Musk announced X Money for April with crypto integration unconfirmed, while MrBeast got USD 200 million for his financial (crypto including) plans from Bitmine.

Trump family crypto dealings deepened — an Abu Dhabi fund took 49% of World Liberty Financial for USD 500 million. But not all families were united by the cryptoasset magic. For example Marc Syz left his family's Swiss bank over bitcoin disagreements.

What to watch in Q2

- IPO pipeline resolution. With Kraken, OKX, Bitpanda, and potentially Ledger all in various stages of public listing plans, Q2 will test whether market conditions improve enough for any to proceed — or whether more will freeze.

- Tether audit progress. The KPMG and PwC engagement is the single most important transparency event in stablecoin history. Any signals about scope, timeline, or early findings might move the entire stablecoin market's credibility.

- X Money cryptoasset integration. If Musk's payments platform launches in April as announced, whether it includes bitcoin or crypto functionality will be one of Q2's most consequential corporate decisions for adoption.

- Reserve company survival. If bitcoin stays depressed, the gap between companies with functional business models (the Steak 'n Shake template) and pure treasury plays (the Nakamoto cautionary tale) might widen further. Expect more M&A and restructuring.

Exchanges

Crypto exchanges raced to become full-stack financial platforms — partnering with Wall Street, launching stocks, prediction markets, and AI tools — while MiCA filtered out weaker players, and deteriorating market conditions froze IPO ambitions.

Key trends & patterns

- Exchanges are sprinting to become "everything apps" — adding stocks, prediction markets, AI agents, social features, lending, and pushing into banking territory, with one gaining direct Fed access for the first time.

- Traditional finance players are launching their own crypto-adjacent products, intensifying competition from both sides.

- Wall Street is no longer watching from the sidelines — it's investing directly in and partnering with crypto exchanges.

- IPO plans froze across the board as market conditions deteriorated and pre-IPO costs mounted.

- MiCA is actively filtering the EU market, banning even licensed operators who can't maintain compliance.

- Layoffs hit multiple major platforms, signaling a sector-wide cost correction despite product expansion.

The dominant Q1 story was exchanges racing to outgrow their crypto-only origins. Coinbase declared an "everything exchange" vision — crypto, stocks, commodities, prediction markets — but spent the quarter fielding criticism over customer service, security flaws, a failed SocialFi experiment, and accusations of lobbying against bitcoin tax exemptions. Binance added gold and silver futures. Bitpanda launched stock and ETF trading. OKX went furthest, building an in-app social network and AI trading agent tools; Crypto.com moved similarly on AI agents and prediction markets. LMAX launched Omnia Exchange, combining forex and cryptoassets in a single venue. Traditional incumbents pushed in too — Cboe entered prediction markets, CME Group floated issuing its own token.

Wall Street placed direct bets: NYSE parent ICE invested in OKX at USD 25 billion; Kraken partnered with Nasdaq; Franklin Templeton explored tokenized collateral with Binance. Most dramatically, Kraken became the first crypto company to access the Fed's payment system — provoking immediate banking industry backlash.

Yet IPO momentum stalled. Kraken shelved its listing, OKX delayed until returns could be guaranteed, and Bitpanda — despite 16% revenue growth and 25% user growth — saw EBITDA crater 75% amid pre-IPO spending. Bullish posted a USD 564 million loss. Layoffs followed: Gemini cut 30% of staff while retreating from the EU entirely; Crypto.com cut 12%.

On the communication front, the biggest exchange, Binance, had a busy quarter too dominated headlines — OKX founder Star Xu accusing it of destabilizing markets, a WSJ lawsuit, an Australian fine, old-new insolvency rumors, public account closures, and the Bifinity MiCA saga in Lithuania while seeking a MiCA licence in Greece. The exchange countered with transparency moves: requiring market maker disclosure and converting its protection fund to bitcoin.

MiCA continued reshaping Europe's map. KuCoin was banned despite holding an Austrian license after losing its AML team. Bybit and Bifinity were blocked in Lithuania on national security grounds, triggering a backlash from local investment and business community. Operational risks persisted elsewhere — Bithumb accidentally sent essentially fake BTC 620,000 (USD 43 billion) to clients before recovering nearly all of it, while OKX had to address complaints about a frozen account tied to identity fraud.

What to watch in Q2

- Reshaping market: Most likely, we’ll see more signs that crypto and traditional trading platforms integrate one another services, pushing new partnerships and competition even further.

- Super-app fatigue vs. traction: Exchanges are launching social networks, AI agents, prediction markets, stocks, and lending simultaneously. Q2 might offer first signs which of these product bets gain actual user traction versus becoming costly experiments like Coinbase's SocialFi.

- IPO window: Will improving conditions (if they improve) unfreeze Kraken and OKX listings — or will the diversification race demand even more capital before going public?

- Banking-exchange collision: Kraken's Fed master account sets a precedent. Watch whether other exchanges pursue similar access and how banking lobbyists respond legislatively.

- MiCA enforcement tightening: After KuCoin's ban, regulators may scrutinize other MiCA holders more aggressively — particularly on AML staffing and operational readiness.

Prediction markets

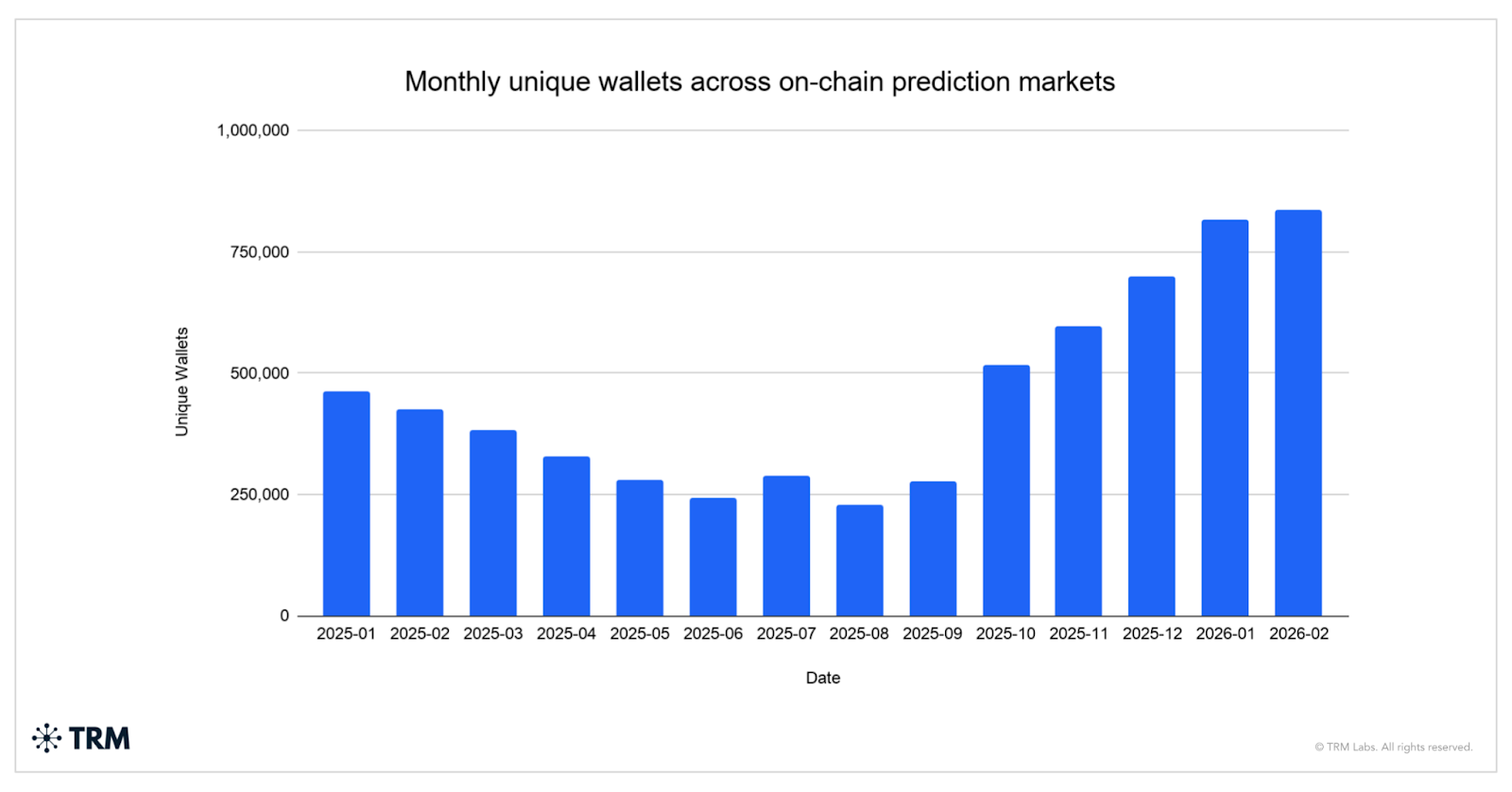

Prediction markets went from a niche crypto curiosity to a USD 20 billion-a-month industry — and the data now shows most participants are worse off than if they'd just used a bookmaker.

Key trends & patterns

- Monthly volume hit USD 20 billion — twenty times more than a year ago, with 800,000+ wallets trading each month.

- New platforms keep launching, but Polymarket still dominates while expanding into new asset classes like real estate.

- Research shows only whale-sized traders beat traditional bookmakers — everyone else loses more here than at a sportsbook.

- Manipulation is becoming a feature, not a bug — insiders are monetizing advance knowledge of news and even criminal investigations.

- Some European regulators are banning prediction markets outright, while the US Fed publicly endorsed them as useful forecasting tools.

- Bitcoin-native alternatives appeared, settling bets in satoshis instead of stablecoins.

The headline number is hard to ignore: monthly trading volume in prediction markets hit USD 20 billion in January 2026, roughly twenty times the figure from a year earlier, with over 800,000 unique wallets participating each month. CertiK put the 2025 annual volume at USD 63.5 billion — a fourfold jump from 2024. By any measure, this is no longer a side show.

But growth attracted exactly the kind of attention that complicates the story. On the supply side, new entrants piled in: Crypto.com launched its own prediction market platform OG, Cboe Global Markets signaled plans to compete, and bitcoin-native alternatives (e.g., PREDYX) appeared, settling everything in satoshis. The space is diversifying away from Polymarket dominance, though Polymarket itself kept expanding — notably into real estate price prediction via a partnership with Parcl.

On the demand side, the picture is less flattering. New research found that only traders deploying at least USD 500,000 outperform traditional bookmakers in prediction markets. Everyone below that threshold loses more here than they would at a sportsbook — which makes the 800,000-wallet participation figure look less like democratized forecasting and more like a new extraction venue. Meanwhile, CertiK flagged persistent manipulation and security problems, and Q1 delivered concrete examples: someone placed a USD 32,500 bet ahead of Venezuela-related news and walked away with over USD 400,000; another participant profited hundreds of thousands by betting on which platform would be named in a criminal manipulation report. Prediction markets are starting to function as a monetization layer for insider knowledge of crypto crime itself.

Regulators noticed. Polymarket was already banned in several European countries. But the US Federal Reserve went the other direction, publicly praising prediction markets as useful tools for gauging expectations around interest rate decisions — a notable institutional endorsement that may shape how US regulators approach the space.

What to watch in Q2

- Actual product launches. Whether Cboe actually launches its product — traditional finance entry would change the competitive and regulatory dynamics significantly.

- Regulatory momentum in Europe. With some EU member states already banning Polymarket, the question is whether this becomes a patchwork or triggers a coordinated EU-level response.

- Retail behavior. How the small-trader loss data influences participation growth — if the research gets traction, the 800,000-wallet number may plateau or the market may bifurcate further into whale-dominated venues.

- Manipulation enforcement. Q1 surfaced multiple cases, but no meaningful consequences, besides platforms trying to introduce preventive mechanisms. If manipulations continue, it undermines the “better than polls" narrative that drove institutional interest.

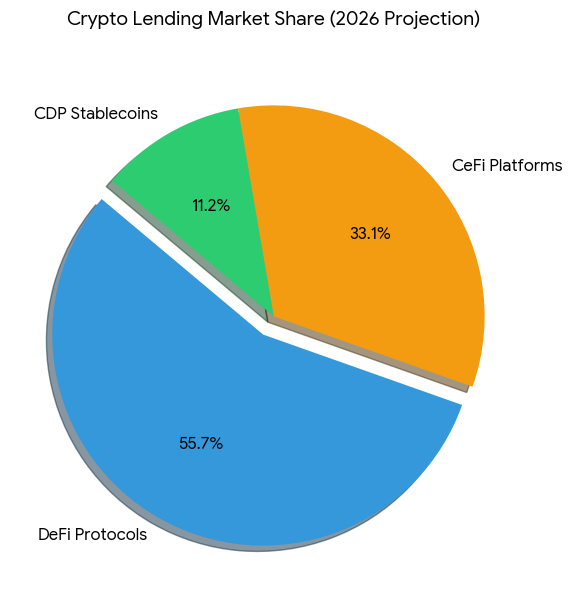

DeFi & CeFi

DeFi, CeFi (centralized finance) and crypto lending grew up fast — loan terms lengthened, rates dropped, BlackRock showed up on Uniswap, and bitcoin mortgages stopped being a joke — but Aave reminded everyone the plumbing still breaks.

Key trends & patterns

- Crypto-backed loan terms are lengthening and rates dropping — the market is shifting from speculative margin to real credit products.

- Bitcoin-native DeFi is expanding, with new protocols enabling smart contracts and staking BTC directly without the usual blockchain workarounds.

- Crypto collateral is entering the traditional mortgage system, backed by government-sponsored entities.

- The biggest DeFi platform had a brutal quarter — oracle failures, user losses, and governance walkouts.

- Traditional finance giants are showing up on decentralized exchanges, slowly destroying the rhetorical wall between TradFi and DeFi.

- Regulators have shifted from "should we engage" to "how do we regulate" — the ECB now openly challenges DeFi's decentralization claims.

- Institutional DeFi products are multiplying, targeting yield without custody surrender — a direct challenge to banks.

The clearest signal this quarter was crypto-backed lending crossing from experimental to structural. DeBiFi data showed average BTC loan durations exceeding 13 months for the first time, with rates falling from 13.55% to 11.18%. Xapo confirmed the trend — 52% of its BTC-backed loans now run 12 months. These aren't speculative margin loans anymore; they're starting to look like actual credit products. Voltage Credit added another dimension by building a credit line on Lightning Network where borrowers can take and repay in USD, blurring the boundary between bitcoin infrastructure and traditional lending rails. BitGo launched a unified digital asset financing platform to give institutions collateralized borrowing and lending capabilities.

The mortgage front moved furthest. Coinbase working with government-backed Fannie Mae on cryptoasset-collateralized conforming mortgages is a different category of legitimacy than anything before it. Newrez confirming it will factor cryptoasset holdings into lending decisions reinforced the direction. This isn't DeFi in the purist sense — it's crypto collateral entering the traditional credit system.

On the institutional side, BlackRock listing tokenized Treasury fund units on Uniswap was the quarter's most symbolically loaded event — the world's largest asset manager using a decentralized exchange. Strategy signaling a shift toward digital asset debt products pointed the same way. Meanwhile, Lombard and Bitwise are launching Bitcoin Smart Accounts specifically targeting institutions that want yield without losing custody.

Bitcoin-native DeFi kept expanding. OpNet launched smart contracts directly on Bitcoin's base layer — no bridges, no wrapped tokens — potentially challenging Ethereum's DeFi dominance if it gains traction. Another BTC staking platform, Babylon raised USD 15 mln. and integrated with Ledger for direct staking from hardware devices.

But the quarter also delivered painful reminders. Aave — by far the dominant DeFi platform — had a rough stretch: a USD 27 mln. liquidation cascade likely triggered by an oracle bug, a user losing ~USD 50 mln. despite on-screen warnings, and a governance crisis with two major contributors walking away. However, the DeFi giant ended the quarter on a high note, releasing its long-awaited v4 on Ethereum, which brings more use cases for institutions while also helping the platform to expand into real-world assets.

The ECB published a report arguing DeFi governance is far more centralized than protocols claim. Well, it has been a public secret for many years now. Both the technical failures and the centralization critique point to the same gap: DeFi’s infrastructure and governance haven’t matured as fast as its ambitions. Not to mention the multimillion security incidents that hit many DeFi platforms last quarter.

What to watch in Q2

- Crypto mortgage traction. How the Coinbase/Fannie Mae plans progress and on what terms. If conforming mortgages accept crypto collateral with stable loan conditions regardless of price drops, it changes the asset class narrative.

- Bitcoin-native DeFi adoption. OpNet and Babylon both launched ambitious products — Q2 will show whether bitcoin holders actually use them or whether Ethereum now has another serious competitor.

- Institutional DeFi regulation. The ECB's centralization critique likely foreshadows regulatory proposals. Watch for concrete EU moves to bring DeFi governance under oversight frameworks.

- Aave v4 reinvestment module. If it puts ~USD 6 mlrd. in idle platform assets to work, this would be a significant test of whether DeFi can manage passive capital at scale without new risk blowups.

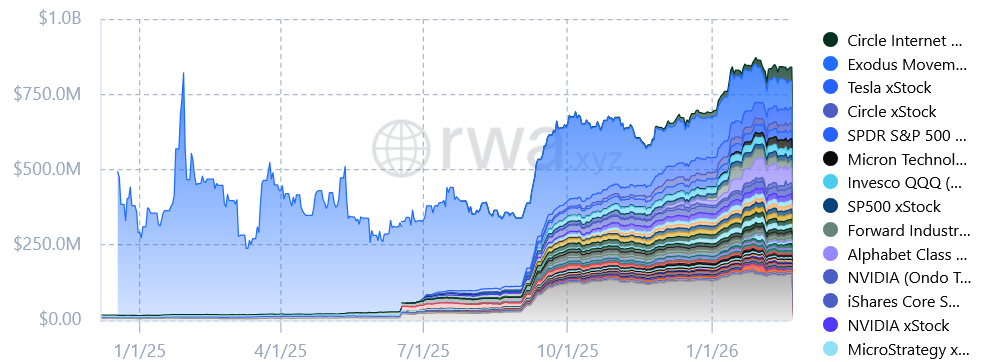

Tokenisation

Tokenization graduated from pilot projects to institutional production as trillion-dollar asset managers, major exchanges, and central banks committed real capital and infrastructure to putting traditional assets on-chain.

Key trends & patterns

- Trillion-dollar asset managers moved from tokenization pilots to actual product launches this quarter.

- The US now has a regulated path for trading tokenized securities on a major exchange.

- Europe's central bank committed to a multi-year tokenized finance roadmap, but still seemingly trails the US in execution speed.

- The range of tokenized assets kept widening — from treasuries and equities to gold, real estate, bank deposits, and even mining products.

- Tokenized stocks became available to retail users through popular crypto wallets.

- At Davos, tokenization and stablecoins drew more institutional attention than Bitcoin itself.

The striking pattern in Q1 was the sheer weight of the institutions now moving. BlackRock listed tokenized US treasury fund units on Uniswap, then its CEO declared that tokenized funds will do to finance what the internet did to postal mail. Franklin Templeton (USD 1.7 trillion AUM) partnered with Ondo Finance for 24/7 trading of traditional instruments and separately explored tokenized assets as collateral with Binance. Amundi, Europe's largest asset manager, launched a EUR 100 million tokenized fund on Ethereum and Stellar. Invesco took over Superstate's USD 900 million tokenized fund. These are no longer experiments — they are product launches by firms managing trillions.

On the infrastructure side, the SEC approved Nasdaq to trade tokenized securities — arguably the quarter's most consequential regulatory move for the category. IronLight raised USD 21 million for a regulated tokenized securities marketplace. BitGo and zkSync began building tokenized deposit infrastructure for banks, while Bitpanda launched its own blockchain aimed at helping banks develop tokenized asset products. In Japan, SBI and Sony invested USD 63 million into Startale for tokenized finance expansion.

Europe is trying not to fall behind. The ECB is working on a multi-year tokenized finance plan targeting 2028, with a technical solution due Q3 2026. Swiss bank AMINA joined 21X, Europe's first fully regulated DLT trading venue. European DLT operators, including Lithuanian Axiology (which raised USD 5 million in seed funding), publicly urged the EU to move faster or lose ground to the US. At Davos, tokenization and stablecoins received more attention than Bitcoin itself — a telling signal about where institutional minds are focused.

The range of assets being tokenized also widened noticeably. Gold saw action from both Tether (launching fractional Scudo units for its XAUT gold token) and the World Gold Council (building shared infrastructure to challenge Tether and Paxos). Real estate entered the picture with Cardone Capital announcing plans to tokenize its USD 5 billion portfolio and Bed Bath & Beyond acquiring Tokens.com. Apex Group tokenized a Bitcoin mining product. MetaMask began offering 200+ tokenized stocks to US users, and Robinhood tested its own blockchain for tokenized asset trading. The Reserve Bank of Australia endorsed tokenization trials as carrying "revolutionary" potential.

What to watch in Q2

- From plans to results: Q2 might reveal whether all of the above plans and announcements are turning into something more specific, with first results possibly demonstrating market demand for so many new options.

- Trading 24/7: Increasing abilities to trade traditional assets 24/7 as their tokenized versions might substantially affect both the traditional markets and cryptoasset market, which are already open 24/7.

- ECB's Q3 technical solution deadline approaches — any delays or scope changes will signal whether Europe's tokenization ambitions are real or aspirational.

- Blockchain competition: How will the new tokenization project affect Ethereum’s dominance in this market and whether other blockchains get a bigger share in this tokenized pie.

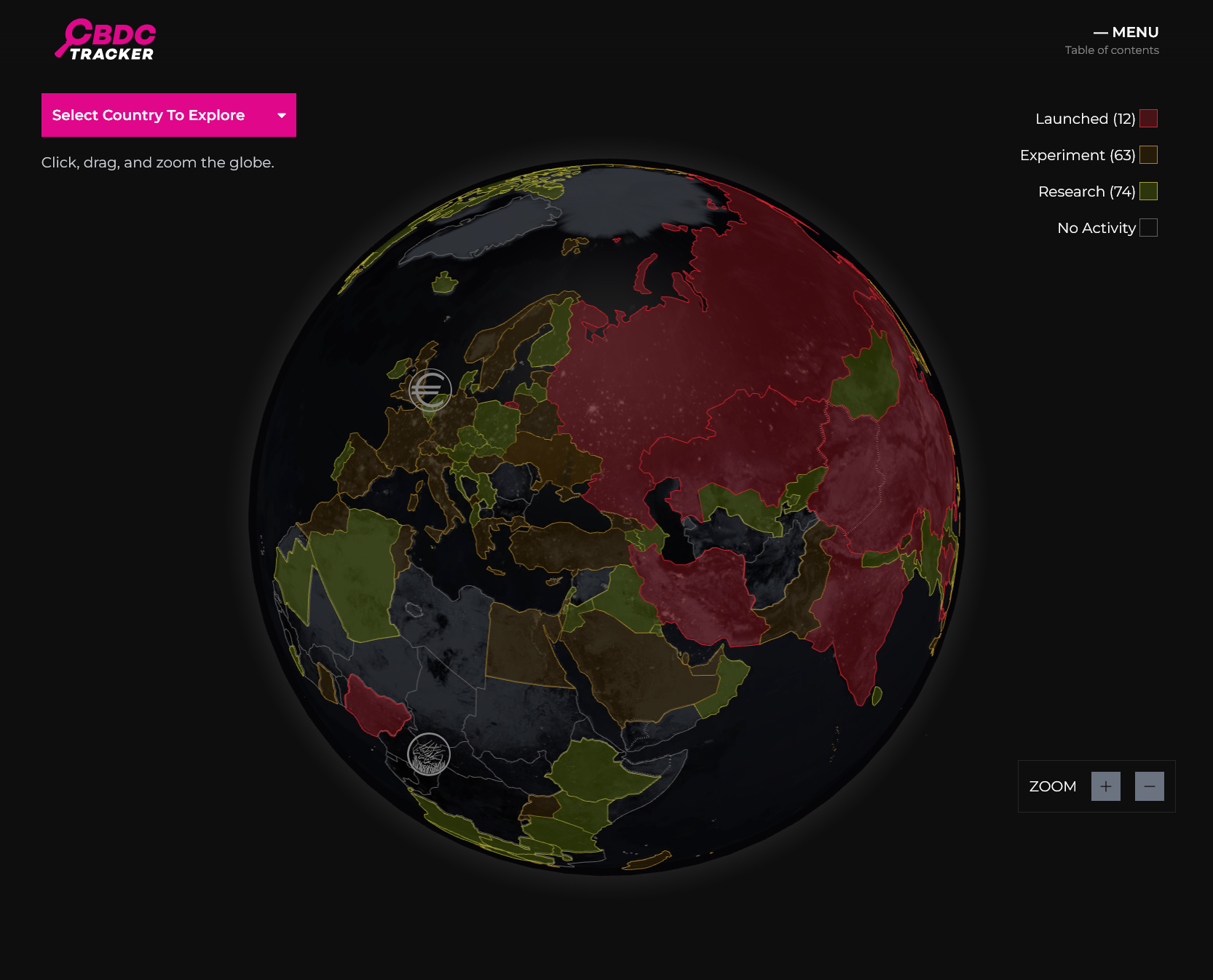

CBDC

While most of the world quietly walks away from CBDCs, the ECB doubled down on the digital euro — hiring experts, courting partners, and increasingly framing stablecoins as a threat to justify its own relevance.

Key trends & patterns

- Most central banks are abandoning CBDCs; the digital euro is increasingly an outlier project, not a global trend.

- The U.S. explicitly ruled out a digital dollar, isolating the few remaining CBDC proponents.

- The ECB accelerated hiring, partner searches, and standard-setting — building institutional momentum to make the project harder to cancel.

- The core ECB narrative shifted to framing stablecoins as a systemic threat requiring a CBDC "trust anchor" — a claim the market isn't validating.

- Political backing exists on paper, but the project's justification increasingly relies on warning against alternatives that already work.

The defining dynamic of Q1 was divergence. The global CBDC wave that peaked a few years ago continued to recede — more central banks shelved their projects, and the U.S. Fed made clear it sees no point in a digital dollar. That leaves the ECB in a somewhat awkward company: China, India, and Russia are the only other major jurisdictions adopting CBDCs.

Yet rather than pause and reassess, the ECB accelerated. The quarter saw a steady drumbeat of operational moves: a call for payment companies to join digital euro testing, a search for experts to integrate it into ATMs and card terminals, a privacy hire, and signals that technical standards could drop within months. A pilot is now targeted for 2027 H2. The Pontes initiative, meant to bridge blockchain and traditional payment rails, advanced in parallel. None of this is new — the digital euro has been in preparation for years — but the pace of hiring and partner-seeking suggests the ECB is trying to create enough institutional momentum to make the project politically irreversible.

The most telling pattern, though, is the narrative. The ECB spent Q1 relentlessly arguing that stablecoins threaten the eurozone's monetary sovereignty and that a CBDC is needed as a "trust anchor" for tokenized finance to scale. ECB board member Piero Cipollone made this case explicitly in late March. This looks more like desperation than conviction — and it’s hard to argue with: the stablecoin market is growing fine without a central bank backstop. The European Parliament and 70 economists offered political cover, but the core tension remains. The ECB is building a product that most of the world has decided it doesn’t need, and justifying it by warning against the private-sector alternatives that are already working.

What to watch in Q2

- Digital euro technical standards release. If published, this would be the first concrete spec businesses can build against — and the first real test of whether the private sector sees enough reason to engage.

- Christine Lagarde's position. Speculation about her possible early departure before 2027 matters because the digital euro is closely tied to her leadership. A change at the top could stall or reshape the project.

- Stablecoin growth vs. ECB rhetoric. If euro-denominated stablecoins keep growing (they've already recovered from Tether EURT's EU exit), the ECB's "trust anchor" argument gets harder to sustain.

- China's digital yuan signals. The unconfirmed story about an automatic fine deducted from a CBDC wallet in China went viral in January. More stories like this — whether verified or not — will shape public perception of what CBDCs actually enable.

Mining

Miners spent Q1 bleeding cash on AI bets that haven't paid off, selling bitcoin to stay afloat, while the industry's self-correcting economics and expanding energy partnerships quietly proved the core business isn't going anywhere.

Key trends & patterns

- Miners' AI pivot is burning cash faster than it's generating revenue — the bet hasn't paid off yet.

- Miners are selling bitcoin to fund AI infrastructure, among other things, pressuring the market.

- Mining costs now rival market prices for some operators, squeezing margins to near zero.

- Hashrate ended Q1 down 7% from January but up 22% year-over-year.

- Energy companies worldwide keep adopting mining to absorb surplus power and balance grids.

- Mining-as-heating is maturing — greenhouses, homes, and even 3D printers now run on mining waste heat.

- Some miners are diversifying into altcoin mining and new financial products connecting miners with investors.

- One pool controlling a third of hashrate found seven consecutive blocks, reigniting concentration concerns.

- Open-source mining software and solo mining hardware keep pushing decentralization at the grassroots level.

The dominant story of Q1 was the collision between miners' AI ambitions and financial reality. MARA Holdings posted a $1.7 billion loss, Hut 8 lost $248 million, and TeraWulf saw revenues rise but losses widen. Research from Wintermute and CoinShares confirmed the pattern: AI revenue is growing slower than expected, and the pivot is expensive. Bitfarms rebranded to Keel Infrastructure to signal a broader identity shift, but the sector as a whole is selling bitcoin reserves not out of panic, but to fund AI infrastructure capex, besides their daily operations. For some miners, the cost of producing a bitcoin now roughly equals just buying one on the open market, while for others buying bitcoin is now cheaper than mining it.

Hashrate reflected the turbulence. After fluctuations throughout Q1, Bitcoin hashrate ends the quarter 7% lower than on January 1, but still 22% higher than a year ago. The self-correcting mechanism held: as weaker miners dropped out, conditions improved for those who stayed.

Meanwhile, energy companies kept expanding the mining-as-grid-tool thesis. Engie in France explored mining at a Brazilian solar plant to absorb surplus power, Eskom in South Africa moved to sell excess daytime electricity to miners. The heating use case matured too — Canaan tested a 3 MW greenhouse heating project in Canada, Bitcoin-heated communities stayed warm in Finland, and someone built a 3D printer prototype that mines Bitcoin with its own waste heat.

Diversification went beyond AI. Foundry announced an institutional Zcash mining pool launching in April, and Bitdeer shipped hardware for Litecoin and Dogecoin mining. New infrastructure emerged: Tether released open-source MiningOS, the Mezzamine platform launched to connect miners with yield-seeking investors at 8–9% returns, and BIP 54 — a proposal to help miners pack blocks more efficiently — was successfully tested on mainnet.

The quarter also surfaced a concentration concern. Foundry, controlling roughly a third of hashrate, found seven consecutive blocks, triggering a rare block reorganization and reigniting debate about how many confirmations are truly enough.

What to watch in Q2

- Mining profitability pressure. If bitcoin prices don't recover meaningfully, the BTC-selling cycle might intensify — the question is how much additional sell pressure the market can absorb before the weakest miners capitulate and difficulty resets in survivors' favor.

- Bitcoin vs. AI dynamics. Fast-growing demand for AI computing and BTC market dynamics will affect Bitcoin miners diversification plans.

- New models. What new models, revenue streams besides AI miners will implement to make their revenues more sustainable and increase profits.

- Starcloud's planned orbital mining test. If bitcoin mining hardware actually operates in space this year, it opens a genuinely novel cost structure discussion.

- The asynchronous AI computing market. If AI workloads become flexible enough to switch on and off like mining rigs, miners might lose their key advantage as grid-balancing partners in some areas. However, even in this case, Bitcoin has serious advantages.

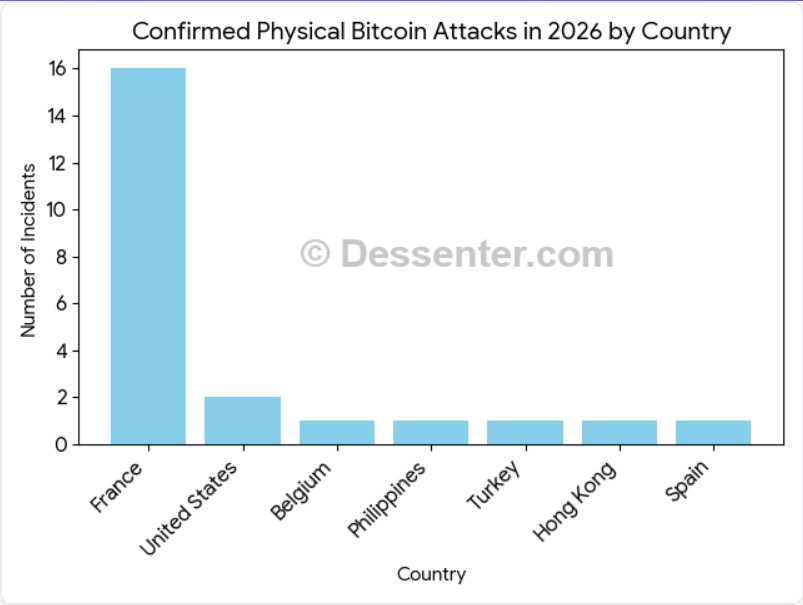

Crime

Crypto crime went industrial in Q1 — criminals are now running their operations as businesses, physical attacks on holders surged, and AI-powered scams increased.

Key trends & patterns

- North Korea is running a national-scale crypto extraction industry, hitting major platforms in serial fashion.

- Physical attacks on crypto holders surged 75%, with Europe — especially France — as the most dangerous region.

- AI is materially scaling scam operations, boosting impersonation schemes and overall criminal efficiency.

- Social engineering remains devastatingly effective, with individual losses reaching hundreds of millions.

- New scam vectors keep emerging — fake stablecoins, weaponized political debates, crypto ATM fraud.

- Traditional banks face legal consequences for enabling crypto fraud, not just crypto-native firms.

- Law enforcement scores occasional wins but remains systemically outpaced by the crime wave.

The quarter's defining pattern is professionalization across every category of crypto crime. North Korea's Lazarus group didn't slow down: they struck again in March, hitting major BTC and crypto-powered marketplace Bitrefill and disrupting its operations for roughly two weeks while also emptying the company's cryptoasset wallet. These are no longer isolated incidents; North Korea is running what amounts to a national extraction industry.

On the streets, the picture is equally grim. There were at least 23 registered physical attacks on cryptoasset holders in Q1, or 2 more than in Q1 2025. However, the real scale is not known, as multiple cases are not being reported. To compare, there were 72 confirmed cases in 2025, a 75% increase year-over-year, with Europe — particularly France — as the most dangerous region. Q1 alone brought a kidnapping attempt in Madrid, a home invasion in France by criminals posing as police.

In other crime news, there was a bizarre domestic case in the UK where a husband accused his wife of stealing USD 172 million in bitcoin by reading his seed phrase through CCTV cameras. The message is clear: if you're visibly wealthy in crypto, you're a target in ways that traditional wealth holders rarely face.